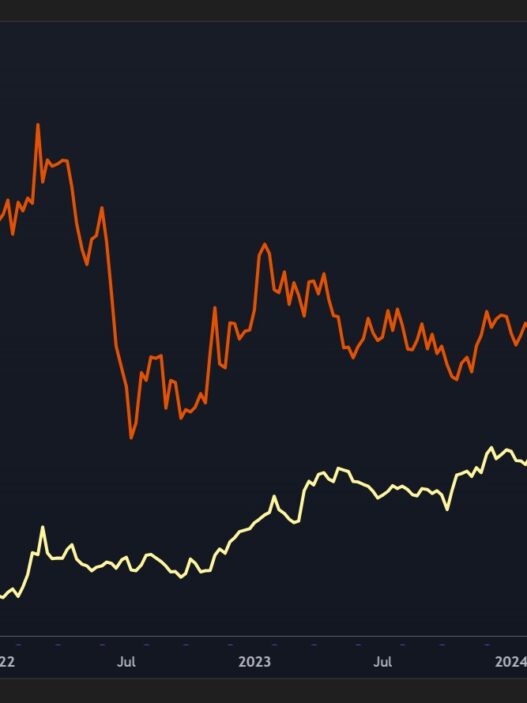

Copper futures prices are up 13% in the last 2 months, rising from $8,483 in early February to now $9,560 USD/t. As having broken the (red) resistance recently, a longer-term upward trend is anticipated.

“Open interest on copper has SKYROCKETED in March on the back of increased Chinese stockpiling. Has China set the stage for a bull-run in copper? Markets doesn‘t really seem to care what China needs the copper for, only that they buy it.“ (Source)

“The fundamental outlook for copper is improving faster than we had previously anticipated. Based on our supply and demand forecasts, the copper market is entering an extended period of deficits now. We expect this to lead to declining inventories and higher prices sooner than we had previously anticipated. The supply response to these higher prices will take too long to balance the market as the lead time to bring new capacity online is 5+ years for brownfields and 10+ years for greenfield projects. If growth in supply lags growth in underlying demand, as we expect, then demand destruction will be needed for the market to balance. This demand destruction will require a significantly higher price. Ultimately, we believe the copper price will need to rise enough to incentivize the development of new greenfield projects that the world will need to meet demand, but that incentive price is well above $5/lb. If copper goes from $4/lb to $6/lb, as we expect over the next 2-3 years, copper mining equities should roughly double, on average. This leverage to the copper price in a cyclical upturn is clearly the reason to own the equities, in our view.“

Jefferies Group

“Perennial copper supply deficit materializing. As of mid-2023, our house view was that the copper market would be in a slight surplus in 2024 and 2025. On the back of widespread copper concentrate supply disruptions and delays in the ramp of new mine projects, the copper supply balance has changed quickly and our commodity team is now forecasting a shortfall in 2024 and significantly higher deficit conditions throughout the rest of the decade.“

Morgan Stanley

“Traders are betting on a tighter copper market in coming months, as disappointment over China’s stumbling economic growth is overtaken by fears of a squeeze on global supplies... But many traders are placing bets on supply shortages as production cuts by miners begin to take effect. Macquarie has revised down its copper supply forecast by 1mn tonnes for 2024 since last September. Lower production is likely to have a lagged ripple effect through the supply chain. Many copper smelters, which refine the raw material into metal, have become lossmaking as there are too many facilities fighting over a tight supply of raw material. Traders are betting some will have to slow or halt production, tightening supply of refined metal and translating into higher prices in coming months. Goldman Sachs has predicted that copper prices will hit $10,000 per tonne by the year-end on robust Chinese demand and the “ongoing supply-side shock”. Chinese copper smelters are working on a joint plan to cut output to cope with the raw material shortage. News of the rare move earlier this month sent the benchmark copper price soaring above $9,000 per tonne. The volatile rally was further fuelled by speculative trading by hedge funds and others, which built net long positions on the expectation of a tighter market.“ ... “Elevated mine supply disruptions point to a deficit of 700,000 tonnes, and should start to feed through to refined production too,” said Morgan Stanley in a note, predicting a $10,200 per tonne copper price by the third quarter."

“Traders bet on supply squeeze pushing up copper prices“ (Financial Times, March 30, 2024)

RBC on copper: “Chilean copper mine supply (~30% of global production) continues to trend lower on several factors, including technical challenges and falling grades, particularly at Codelco, which has seen significant declines (-16% y/y on January data). Refined copper output from Chinese smelters continues to climb. The current disconnect between refined and mine production is likely not sustainable with the lack of concentrate availability becoming more of an issue, which could tighten the refined market.“ (Source)

“Copper prices and miners are likely to benefit from the growing supply-demand gap. Some miners in particular are thriving due to the optimistic long-term outlook for copper demand. Copper’s strategic importance has driven significant M&A (merger and acquisition) activity in 2022-2023, with major mining companies like BHP and Rio Tinto acquiring copper miners at substantial premiums. Automakers […] are also investing directly in mining companies.“ (Source: “Copper: Wired for the Future“, February 2024)

The gold price is up 15% since mid-February, rising from $1,995 to now $2,300 USD/oz. As having broken the multi-year (red) resistance at the $2,075-level, a longer-term upward trend is anticipated:

Junior gold miners, as shown with the VanEck Junior Gold Miners ETF, are finally following the gold price action and started its own strong upward trend by breaking the (green) resistance, with the subsequent pullback confirming it as new support and starting to accelerate upwards (“thrust“):

“On average, historically, when a major mining company has acquired an explorer, they have done so at 22% of the resource value as we have shown in the chart... As Warren Buffett advises, “It’s crucial to understand that stocks often trade at truly foolish prices, both high and low. ‘Efficient’ markets exist only in textbooks.” It is the best value and macro timing opportunity that I have seen in my career to be rotating out of crowded overvalued large-cap tech stocks and into the mining industry...“

www.crescat.net/a-macro-shift-at-hand/

“Western investor flows look like they are poised to return to gold [...] which include a probable M&A cycle as the major mining companies are in desperate need of scalable new discoveries to replace their dwindling reserves. They will need to acquire or do deals with companies [...] with sizable economic deposits if they do not want to die of old age... Given the US government debt and deficit problem, the likely government Keynesian fiscal and monetary stimulus response to the coming likely tech bust and recession should be the catalyst for one of the highest inflationary periods in US history along to go along with one of its biggest commodity bull markets ever... We believe the distressed value opportunity in the mining industry is creating an excellent entry point...“

www.crescat.net/a-macro-shift-at-hand/

Stephan Bogner

Contact

Rockstone News & Research

Stephan Bogner (Dipl. Kfm., FH)

Müligässli 1, 8598 Bottighofen

Switzerland

Phone: +41-71-5896911

Email: info@rockstone-news.com

Disclaimer: This article is for informational purposes only and does not constitute investment advice or a recommendation to buy or sell commodities. The author holds physical gold and silver, stored in Central Switzerland through Elementum International AG. The author does not hold any direct interests or financial instruments related to other commodities or companies mentioned in this article. All views and forecasts reflect the state of knowledge at the time of publication and are subject to change. There is no guarantee that future developments will unfold as described. Investing in commodities involves risks. Consultation with a licensed financial advisor is strongly recommended.