Today, Homerun Resources Inc. announced an amendment to its previously disclosed non-binding offtake arrangement with Brazilian photovoltaic module manufacturer Sengi Solar Importação e Exportação Indústria e Comércio, under which the anticipated supply of solar glass has been substantially increased.

The amended terms raise the minimum annual volume from 20,000 to 100,000 tonnes, while maintaining the agreed price of 750 USD per tonne, free on board (FOB), at Homerun’s planned solar glass manufacturing facility in Belmonte, Bahia, Brazil.

The revised agreement follows the original offtake framework established in February 2025 and reflects changes in both market conditions and project development since that time.

In particular, the increase in minimum volumes corresponds with rising domestic demand for solar components in Brazil, shifts in trade and tariff structures, and continued progress on Homerun’s solar glass project at the technical and commercial level.

Although the offtake remains non-binding, the expanded volume profile provides a clearer indication of potential demand scale and supports ongoing work related to plant sizing, utilization assumptions and economic modeling.

As such, the amendment contributes to the commercial context underpinning Homerun’s advancement toward a Bankable Feasibility Study (BFS) for its proposed solar glass manufacturing operation.

Brazil’s Solar Market: Scale and Momentum

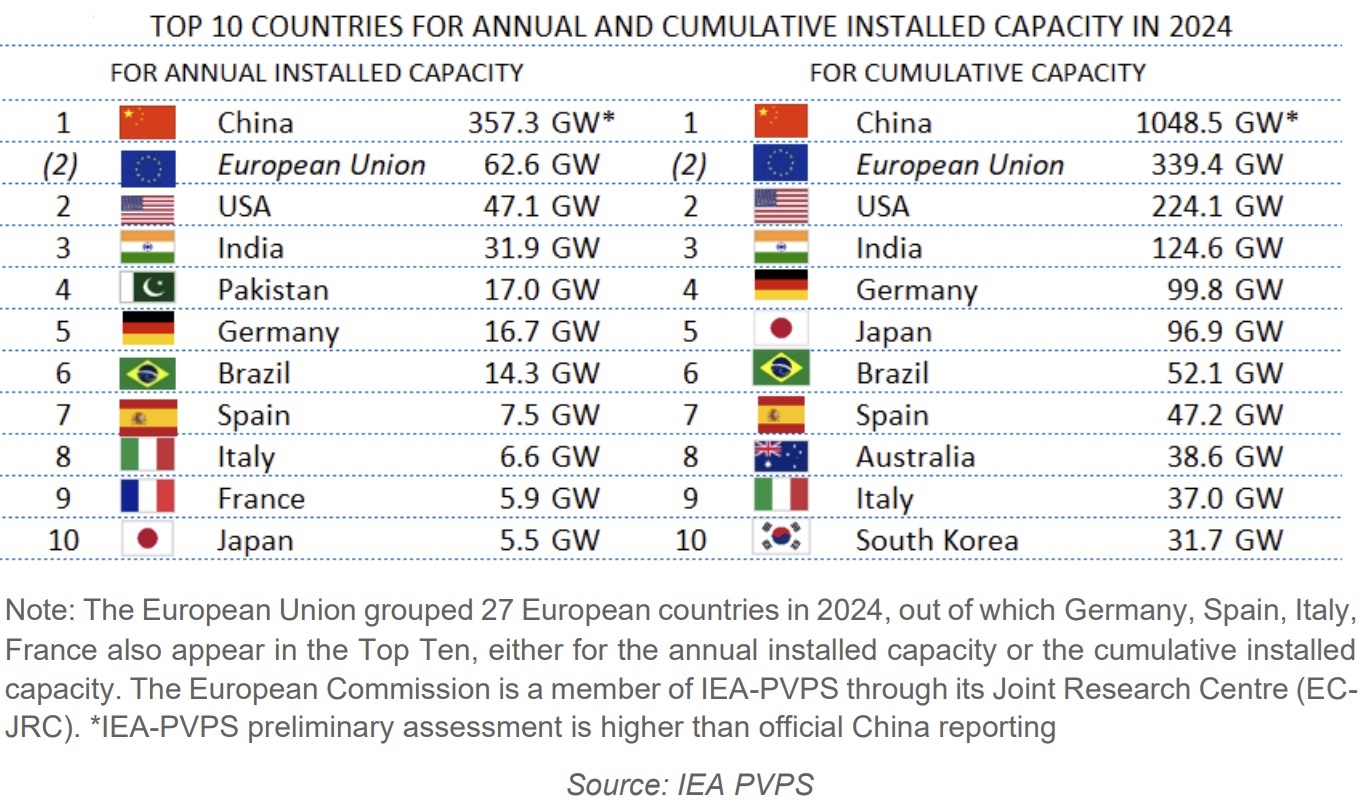

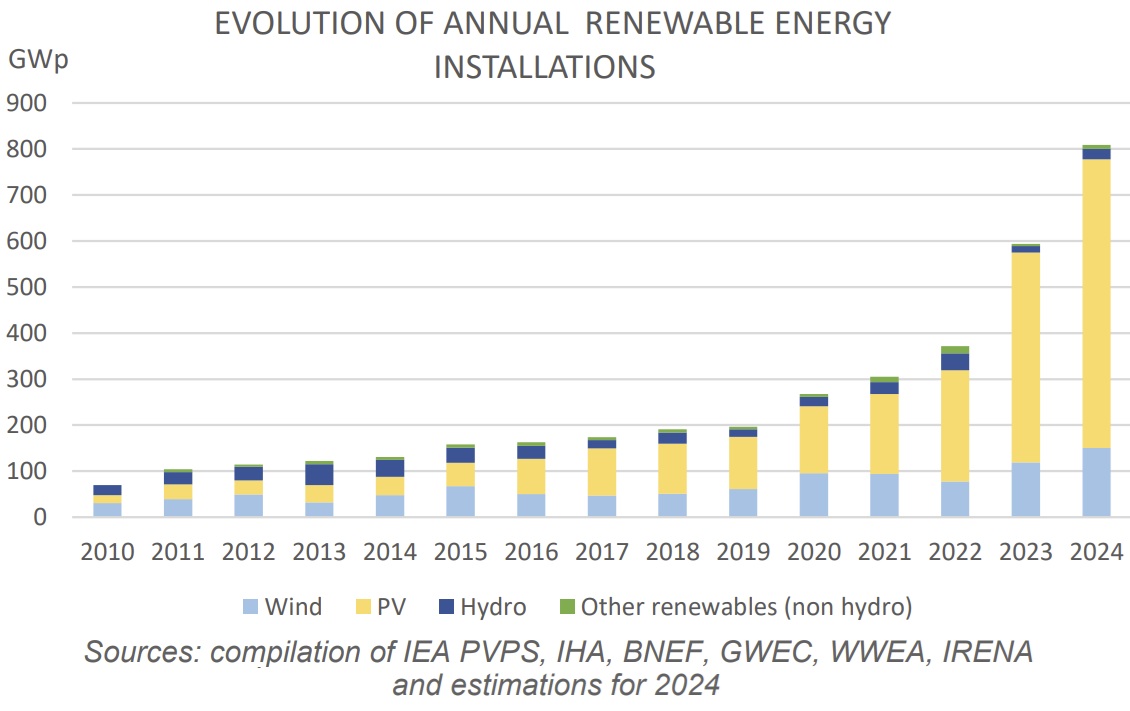

Brazil has established itself as one of the fastest-growing solar markets globally.

According to data from ABSOLAR (Brazilian Solar Photovoltaic Energy Association) and Brazil’s energy regulator ANEEL, the country’s installed solar capacity surpassed 60 GW in 2025, positioning solar as the second-largest source of installed power capacity in Brazil and accounting for ~23% of the national electricity mix. Growth has been driven by both distributed generation, particularly residential and commercial rooftop systems, and continued additions of utility-scale solar projects.

Recent capacity additions further highlight the pace of expansion in Brazil’s power sector. According to Industrial Info Resources (January 21, 2026), Brazil added ~7.4 GW of new installed generation capacity in 2025, with renewable sources accounting for the majority of additions. Solar projects alone contributed around 2.8 GW, while Bahia ranked among the leading states for new capacity brought online during the year. Looking ahead, ANEEL data indicate that a further 9.1 GW of new capacity is expected to enter operation in 2026, supporting continued growth across the renewable energy segment.

At the utility scale, photovolatic (PV) plants alone exceeded 20 GW of installed capacity by early 2026, based on data published by ABSOLAR and reported by Canal Jornal da Bioenergia (January 21, 2026). Since 2012, large-scale solar development in Brazil has attracted more than 87.7 billion BRL (~23 billion CAD) in investments, generated ~601,000 cumulative green jobs, and contributed around 29 billion BRL (~8 billion CAD) in public revenues, highlighting the sector’s increasing economic and industrial relevance within the national energy system.

Recent project announcements further illustrate the pace of solar development at the regional level. In January 2026, Brazil inaugurated the 100 MW Babilônia Sul PV complex in the municipality of Várzea Nova, Bahia, according to Review Energy. The project, developed with an estimated investment of 485 million BRL (~127 million CAD), forms part of Brazil’s Novo PAC infrastructure program and is connected to the national grid via the Ourolândia II 230 kV substation. Regional authorities reported the creation of more than 4,000 direct and indirect jobs, reinforcing Bahia’s role as a leading center for solar generation in Brazil.

The pace of Brazil’s clean energy expansion has also been highlighted in international coverage. According to reporting by Financial Times (December 16, 2025), wind and solar capacity in Brazil has increased from a marginal share of the power mix a decade ago to represent a substantial portion of total installed generation, supported by cumulative investments estimated at ~78 billion USD. The publication notes that Brazil’s renewable build-out is transitioning from a phase focused primarily on capacity additions toward one increasingly centered on system integration, flexibility and the efficient utilization of renewable output.

Policy responses are beginning to reflect this shift toward system optimization. According to reporting by Bloomberg (January 23, 2026), Brazil is preparing to hold its first auction for grid-scale battery energy storage systems in 2026, marking a formal step toward integrating storage as part of the national electricity system. The initiative is intended to enhance operational flexibility, improve utilization of renewable generation and support the continued expansion of solar and wind capacity. Industry observers view the auction as an initial phase in a broader, multi-year deployment of energy storage infrastructure as Brazil’s power system evolves alongside rising renewable penetration.

Looking ahead, projections from industry consultancies, national planning agencies such as EPE (Empresa de Pesquisa Energética) and international organizations including the IEA indicate continued growth through the end of the decade.

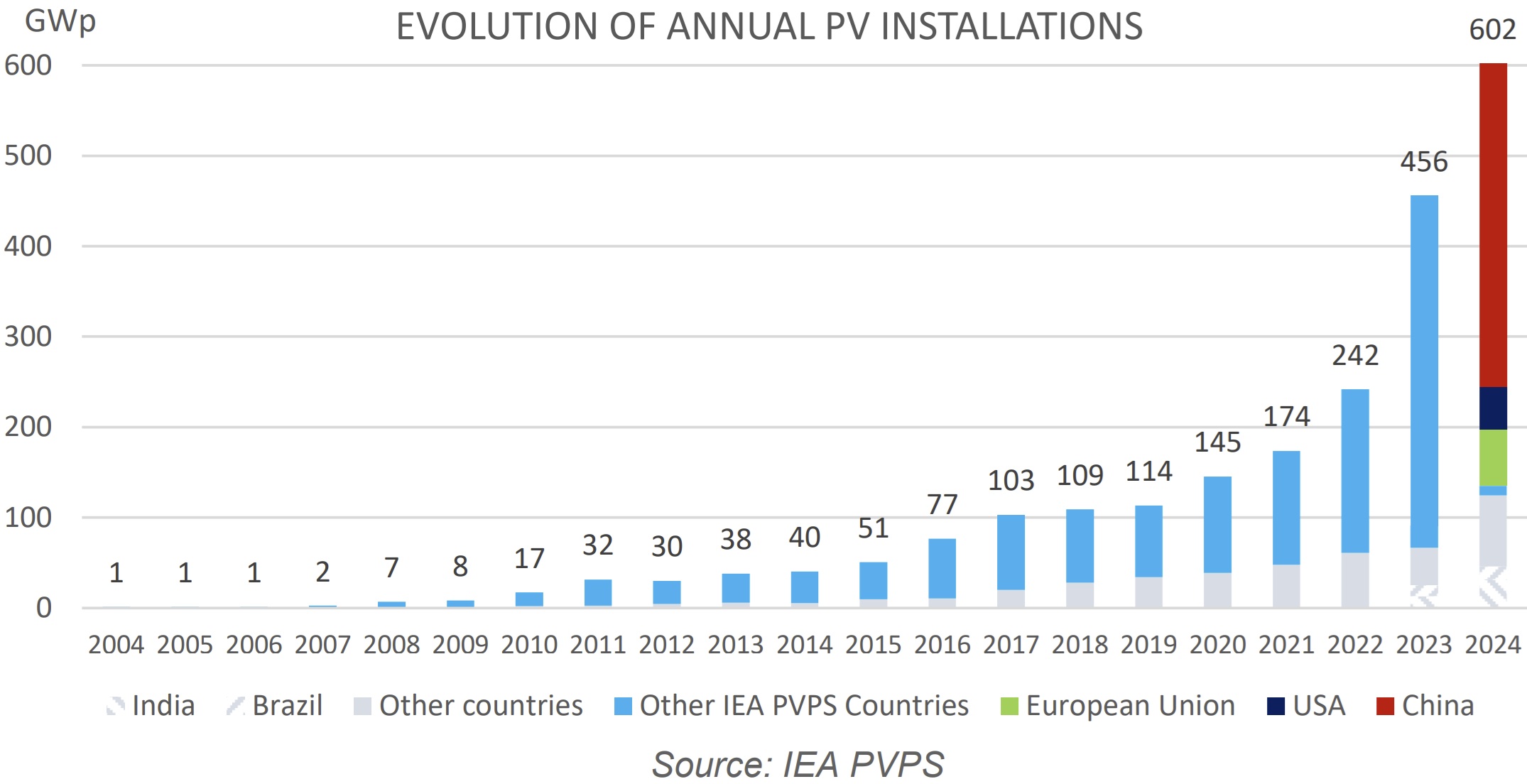

Consistent with this outlook, the IEA’s 2025 Snapshot of Global PV Markets identifies Brazil as one of the world’s leading solar markets, with cumulative installed capacity exceeding 50 GW and annual additions placing it among the top-5 globally.

Depending on policy execution, grid expansion and financing conditions, total installed solar capacity in Brazil is forecast to reach ~90-140 GW by the early 2030s. In this context, solar energy is expected to play an increasingly central role in diversifying Brazil’s historically hydro-dominated power system, particularly during periods of hydrological volatility and drought risk.

This sustained expansion has direct implications for the PV supply chain. As domestic module manufacturing continues to scale, demand for upstream inputs, notably solar glass (one of the most critical and capital-intensive components of PV modules) is expected to increase in parallel with installed capacity growth.

Policy Shifts and Local Manufacturing

Recent developments in Brazil’s trade and industrial policy have further influenced solar supply chain dynamics. As documented by MDIC (Ministry of Development, Industry, Trade and Services) and sector associations, higher tariffs on imported PV components, alongside the reduction or removal of certain tariff exemptions, have altered the cost structure for imported modules and inputs.

These measures have increased the relative competitiveness of locally manufactured solar products, reinforcing policy objectives aimed at strengthening domestic industrial capacity.

As a consequence, Brazilian module manufacturers are placing greater emphasis on secure, in-country sourcing of critical materials in order to manage costs, reduce exposure to logistics disruptions and mitigate trade-related risks.

Within this evolving framework, access to domestically produced solar glass has gained strategic importance.

Against this backdrop, Homerun’s planned 1,000 tonne/day solar glass manufacturing facility in Bahia would represent one of the limited large-scale domestic sources of solar glass in Brazil, supported by locally sourced high-purity, low-iron silica.

German Industrial Expertise and Technology Transfer

Germany has played a foundational role in the development of Brazil’s solar energy sector over the past decade. As documented by GIZ (Deutsche Gesellschaft für Internationale Zusammenarbeit), German public institutions and industrial partners have been actively involved in supporting regulatory frameworks, technical standards and early pilot projects that helped enable Brazil’s solar market to scale. This cooperation included advisory support to Brazil’s energy regulator ANEEL, early grid-integration models for distributed generation and the establishment of technical and vocational training programs supporting renewable energy deployment.

As Brazil’s solar sector has transitioned from early adoption to large-scale industrial deployment, German participation has increasingly shifted from policy support toward industrial technology, equipment and engineering expertise.

A number of German companies have become established suppliers to Brazil’s renewable energy value chain, reflecting the country’s openness to proven industrial technologies and long-term technical partnerships.

Within this context, Homerun’s collaboration with Dorfner Anzaplan and SORG aligns with an established pattern of German-Brazilian industrial cooperation in the solar and materials sectors. Dorfner Anzaplan contributes expertise in industrial minerals processing, silica beneficiation and plant-level process engineering, supporting the transformation of locally sourced high-purity silica into feedstock suitable for solar glass production. SORG, a German specialist in glass furnace engineering and high-temperature industrial systems, provides technology and design capabilities relevant to large-scale solar glass manufacturing.

Together, these partnerships reflect the integration of Brazilian resource availability with German industrial know-how, a model that has underpinned the broader development of Brazil’s solar sector and supports the technical and execution framework underpinning Homerun’s planned solar glass manufacturing facility.

Sengi Solar: A Leading Brazilian Module Manufacturer

Sengi Solar is a privately owned Brazilian manufacturer of PV modules serving residential, commercial and industrial markets. The company focuses on locally manufactured solar products designed to meet Brazilian standards and operating conditions, with an emphasis on durability, consistency and long-term performance.

Sengi’s production lines are designed for high throughput and precision, enabling the manufacture of more than 3,000 modules per day, with individual production processes (including assembly, transformation and inspection) completed in under 25 seconds per module.

The company’s current module portfolio includes products in the 525-555 Wp range, with efficiencies exceeding 21%, optimized for both rooftop and utility-scale solar installations.

The manufacturing platform has been engineered with future adaptability in mind, supporting a broad range of module formats from approximately 440 Wp up to 670 Wp, including bifacial and double-glass technologies.

Sengi places emphasis on automated process control, quality assurance and traceability across its production lines, reflecting broader industrial trends toward scale, standardization and reliability within Brazil’s domestic PV manufacturing sector. The company also maintains long-term performance warranties, compliance with international standards and environmental management practices, including reverse logistics programs for end-of-life module handling.

As Brazil’s solar market continues to expand and local manufacturing becomes increasingly favored, access to dependable domestic supply of key inputs such as solar glass has become an important consideration for module producers. In this regard, Homerun’s intention to supply antimony-free solar glass aligns with evolving ESG expectations around material safety and responsible sourcing.

Within this context, the expanded offtake arrangement reflects Sengi Solar’s interest in aligning future supply with anticipated market demand and domestic production strategies, while supporting the continued scaling of its manufacturing operations.

Integrated Positioning

The amended offtake agreement aligns with Homerun’s vertically integrated strategy linking its high-purity silica resource in Bahia with downstream solar glass manufacturing and Brazil’s expanding domestic solar market.

By strengthening downstream commercial alignment ahead of the BFS, Homerun continues to advance the structural elements required to progress from development toward construction.

Bottom Line

Homerun’s expanded solar glass offtake agreement should be viewed first and foremost as a pragmatic step in aligning upstream resource development with downstream industrial demand in one of the world’s fastest-growing solar markets.

Brazil’s accelerating deployment of both distributed and utility-scale PV, combined with shifting trade policies and a growing emphasis on local manufacturing, creates a clear structural case for domestic solar glass production.

Within this context, the amended offtake provides additional commercial visibility ahead of the BFS while reinforcing the strategic logic of Homerun’s vertically integrated approach.

Beyond solar glass, Brazil’s energy transition is entering a phase where system integration and flexibility are becoming as important as capacity additions. Rising renewable penetration is already driving discussions around grid-scale storage, reflected in emerging policy initiatives and early auction frameworks.

While not required for the current investment thesis, Homerun’s parallel development of long-duration energy storage technology based on silica (the same core material underpinning its Brazilian resource base) represents a potentially powerful strategic option over the medium term. Long-duration storage solutions capable of multi-hour or multi-day discharge could become increasingly relevant as Brazil seeks to manage intermittency, curtailment and seasonal variability across a renewables-heavy grid.

Further out on the horizon, recent durability milestones in perovskite PV modules introduce an additional layer of technological optionality within Homerun’s broader clean-energy platform. Should perovskite technologies mature toward commercial deployment, Brazil’s large, diversified and fast-scaling solar market could ultimately represent a natural downstream opportunity.

Taken together, Homerun’s strategy brings together resources, industrial manufacturing and next-generation energy technologies – anchoring near-term execution in solar glass while preserving exposure to the broader transformation of global energy systems through scalable, de-risked infrastructure.

Company Details

Homerun Resources Inc.

#2110 – 650 West Georgia Street

Vancouver, BC, V6B 4N7 Canada

Phone: +1 844 727 5631

Email: info@homerunresources.com

www.homerunresources.com

ISIN: CA43758P1080 / CUSIP: 43758P

Shares Issued & Outstanding: 73,021,563

Canada Symbol (TSX.V): HMR

Current Price: 0.92 CAD (01/27/2026)

Market Capitalization: 67 Million CAD

Germany Ticker / WKN: 5ZE / A3CYRW

Current Price: 0.57 EUR (01/28/2026)

Market Capitalization: 42 Million EUR

Stephan Bogner

Contact

Rockstone News & Research

Stephan Bogner (Dipl. Kfm., FH)

Müligässli 1, 8598 Bottighofen

Switzerland

Phone: +41-71-5896911

Email: info@rockstone-news.com

Disclaimer and Information on Forward Looking Statements: Rockstone and Homerun Resources Inc. (“Homerun“) caution investors that any forward-looking information provided herein is not a guarantee of future results or performance, and that actual results may differ materially from those in forward-looking information as a result of various factors. The reader is referred to Homerun’s public filings for a more complete discussion of such risk factors and their potential effects, which may be accessed through its documents filed on SEDAR+ at www.sedarplus.ca. All statements in this report, other than statements of historical fact, should be considered forward-looking statements. Much of this report is comprised of statements of projection. Such statements involve known and unknown risks, uncertainties and other factors that may cause actual results or events to differ materially from those anticipated in these forward-looking statements. There can be no assurance that such statements will prove to be accurate, as actual results and future events could differ materially from those anticipated in such statements. Forward-looking statements in this report include expectations related to district-scale control, land tenure and legal certainty, including assumptions that the Company’s mineral rights, long-term lease agreements and surface land positions in the Santa Maria Eterna District will remain in full force and effect, and will continue to provide a legal foundation for long-term operations, infrastructure development and potential industrial-scale manufacturing. Forward-looking statements also include expectations regarding project development, processing and manufacturing, including assumptions that the Company may advance from resource development into large-scale silica processing and downstream manufacturing activities; that processing flowsheets, capital requirements and operating parameters can be defined and optimized through further technical studies, including a Bankable Feasibility Study (“BFS”); and that the scale, quality and continuity of the silica system may support long-life operations and multiple product streams, including solar glass. Forward-looking statements further include expectations related to downstream commercialization and non-binding industrial arrangements, including the expanded non-binding solar glass offtake framework with Sengi Solar. Such statements assume that non-binding arrangements may provide commercial visibility and support technical and economic studies, but may be revised, delayed or not completed, and do not constitute commitments to purchase, finance or construct manufacturing facilities. Additional forward-looking statements relate to product positioning, including assumptions that demand may develop for locally manufactured solar glass, including antimony-free solar glass, in response to evolving ESG standards, trade policies and localization trends in Brazil’s photovoltaic supply chain. Forward-looking statements also include expectations regarding project financing, including assumptions that export-credit-supported financing, government guarantees or comparable mechanisms — particularly in connection with German export credit coverage and Brazilian development banks — may be available, structured on acceptable terms, or successfully combined with other financing sources. Further forward-looking statements relate to infrastructure, logistics and execution, including assumptions that existing and planned transportation infrastructure will support efficient access to and from the Santa Maria Eterna district; that logistics solutions will remain available on acceptable terms; and that development sequencing may be executed in a timely, coordinated and economically viable manner. Finally, forward-looking statements include expectations regarding strategic optionality, including assumptions that the Company’s silica platform may support additional energy-related applications over time, such as long-duration energy storage technologies or advanced photovoltaic materials. Such statements are conceptual in nature and do not represent commitments to commercialize, finance or deploy these technologies. Forward-looking statements are subject to risks and uncertainties including, but not limited to: Land Tenure, Mineral Rights and Legal Risks: Risks related to interpretation, enforcement, renewal, registration and potential legal challenges under Brazilian law that could affect mining, processing or manufacturing activities. Permitting, ESG and Community Risks: Delays, denials or changes to environmental, land-use or operational permits; evolving ESG standards; or community engagement outcomes that may affect project scope, timelines or costs. Financing, Export Credit and Government Support Risks: Uncertainty regarding the availability, timing, structure and economic terms of export-credit-supported financing, government guarantees or incentive mechanisms. Infrastructure, Logistics and Access Risks: Dependence on transportation infrastructure, logistics availability, contractor performance, weather events or changes in government priorities. Execution, Construction and Scale-Up Risks: Risks associated with engineering, construction, commissioning and ramp-up of processing or manufacturing facilities, including cost inflation, equipment delays and workforce constraints. Industrial Partnership and Offtake Risks: Non-binding letters of intent or offtake frameworks may not result in binding agreements, financing or construction, or may be modified or terminated. Technical, Processing and Operational Risks: Differences between laboratory, pilot and commercial-scale performance; variability in throughput, recoveries, energy consumption or operating costs. BFS and Development Risks: Outcomes of technical and economic studies may differ materially from current expectations, affecting project viability or development decisions. Product Qualification and Commercialization Risks: Risks related to customer qualification, specification changes, testing requirements or slower-than-expected adoption of solar glass, including antimony-free products. Market, Pricing and Demand Risks: Volatility in pricing, demand, energy costs, supply-demand balances and macroeconomic conditions affecting silica, solar glass and advanced materials markets. Competitive and Industry Risks: Capacity expansions, pricing pressure, alternative technologies or supply-chain developments by competitors. Regulatory, Trade and Policy Risks: Changes in mining, environmental, tax, trade or industrial policy in Brazil or internationally that could affect project economics or market access. Macroeconomic, Currency and Inflation Risks: Exposure to inflation, interest rates, currency fluctuations and broader economic instability. Force Majeure and External Event Risks: Climate events, natural disasters, pandemics, political instability or labor disruptions. Liquidity and Market Risks: Limited liquidity, volatility or market sentiment unrelated to operational performance. Accordingly, readers should not place undue reliance on forward-looking information. Rockstone and the author of this report do not undertake any obligation to update any statements made in this report except as required by law. Past performance and comparisons to other companies or jurisdictions are provided for illustrative purposes only and should not be considered indicative of future results.

Disclosure of Interest and Advisory Cautions: Nothing in this report should be construed as a solicitation to buy or sell any securities mentioned. Rockstone, its owners and the author of this report are not registered broker-dealers or financial advisors. Before investing in any securities, you should consult with your financial advisor and a registered broker-dealer. Never make an investment based solely on what you read in an online or printed report, including Rockstone’s report, especially if the investment involves a small, thinly-traded company that isn’t well known. The author of this report, Stephan Bogner, is paid by Homerun Resources Inc. On September 8, 2025, Homerun announced that the company “entered into an agreement with Rockstone Research to provide marketing services to the company”, and that “Rockstone Research is an arm’s-length marketing firm and has been engaged for an initial three-month term for total consideration of $25,000, which is payable up front. The company does not propose to issue any securities to Rockstone in consideration for the services to be provided to the company.” The author owns equity of Homerun and thus will profit from volume and price appreciation of the stock. This also represents a significant conflict of interest that may affect the objectivity of this reporting. The author may buy or sell securities of Homerun (or comparable companies) at any time without notice, which may give rise to additional conflicts of interest. Overall, multiple conflicts of interests exist. Therefore, the information provided in this report should not be construed as a financial analysis or recommendation but as an advertisement. This report should be understood as a promotional publication and does not replace individual investment advice. Rockstone’s and the author’s views and opinions regarding the companies that are featured in the reports are the author‘s own views and are based on information that was received or found in the public domain, which is assumed to be reliable. Rockstone and the author have not undertaken independent due diligence of the information received or found in the public domain. Rockstone and the author of this report do not guarantee the accuracy, completeness, or usefulness of any content of this report, nor its fitness for any particular purpose. Lastly, Rockstone and the author do not guarantee that any of the companies mentioned in the reports will perform as expected, and any comparisons that were made to other companies may not be valid or come into effect. Please read the entire Disclaimer carefully. If you do not agree to all of the Disclaimer, do not access this website or any of its pages including this report in form of a PDF. By using this website and/or report, and whether or not you actually read the Disclaimer, you are deemed to have accepted it. Information provided is educational and general in nature. Data, tables, figures and pictures, if not labeled or hyperlinked otherwise, have been obtained from Stockwatch.com, Tradingview.com, Homerun Resources Inc. and the public domain. The cover picture has been obtained and licenced from 123rf.com.