Conceptual rendering of a potential future build-out of Homerun‘s Santa Maria Eterna Industrial Hub. Source: Homerun Resources Inc.

Every industrial empire starts with a first conversion point. For Homerun Resources Inc., that point is no longer theoretical. Today, the company put a price tag on the first industrial facility planned for Santa Maria Eterna: A silica purification plant in Belmonte, Bahia, budgeted at less than 10 million USD.

The planned facility is designed to take raw silica sand from Santa Maria Eterna and upgrade it into a clean, uniform 3N (99.9%) industrial product for customers, for Homerun’s planned solar glass plant and for future 4N and 5N purification stages. In other words, this is where silica sand begins moving up the value chain and taking shape as industrial infrastructure.

While the 9.38 million USD CAPEX estimate may appear modest compared to many mining and industrial projects, the significance of the planned facility lies less in its cost and more in its position within Homerun’s broader industrial architecture.

The 350,000 tonne per year (tpy) plant is designed to become the first purification layer in a 3-phase value add chain and the initial operating bridge between Santa Maria Eterna and future downstream manufacturing. Rather than selling raw silica sand alone, Homerun intends to progressively upgrade its high-purity resource into higher-value industrial products, solar glass feedstock and, ultimately, advanced silica materials.

Where Industrialization Begins

The importance of Phase 1 extends beyond its annual production capacity.

It represents the first physical link between the Santa Maria Eterna resource and the downstream manufacturing ambitions that underpin Homerun’s “Silica Valley of Bahia” vision.

Every subsequent stage of the platform, from solar glass production to future 4N and 5N purification, is expected to rely on a consistent supply of clean, industrial-grade silica generated at this facility.

Viewed through that lens, the planned facility becomes the foundation upon which Homerun intends to build an integrated silica ecosystem. Rather than developing the resource in isolation, the company is establishing the industrial infrastructure required to move further up the value chain and participate in multiple silica-based markets.

In many ways, Phase 1 is the bridge between resource ownership and industrial production.

Turning Silica Into an Industrial Product

The planned facility will process ~350,000 tpy of silica sand, equivalent to roughly 50 tonnes per hour of finished product output.

According to today‘s news-release, the facility is designed around a physical purification flowsheet intended to produce a 3N industrial-grade silica product through a series of mechanical cleaning, sizing and upgrading processes.

The engineering scope developed by Minerali Industriali Engineering Srl (MIE) includes a complete purification circuit consisting of:

- Washing (removing clays, fines and surface contaminants)

- Grading (sizing material into target fractions)

- Sieving (mechanical separation of particles by size)

- Attrition scrubbing (removing coatings and impurities from sand grain surfaces)

- Classification (refining particle-size distribution and product consistency)

- Drying (preparing the final product for storage, handling and transport)

While these steps may sound simple, they serve a critical purpose. The objective is not merely to move sand through a processing plant, but to remove impurities, reduce contamination, improve particle consistency and prepare a reliable feedstock suitable for demanding industrial applications and downstream manufacturing requirements.

Importantly, the Phase 1 circuit disclosed by Homerun is based on physical purification rather than chemical leaching. In many higher-purity silica processing routes, acid leaching may be required to remove more stubborn impurities. By contrast, Homerun’s disclosed 3N process route does not include acid leaching at this stage, which may help explain the comparatively modest CAPEX profile and relatively straightforward Phase 1 flowsheet.

From Concept to Engineering

The purification circuit itself is only one component of the work currently being undertaken. Homerun has engaged MIE to deliver a complete preliminary engineering package for the proposed 350,000 tpy primary silica processing facility. According to the news release, MIE’s mandate includes:

- Development of the project‘s capital cost estimate, completed on June 5, 2026.

- Process flow design for the complete physical purification circuit, including washing, grading, sieving, attrition scrubbing, classification and drying.

- Plant layout and civil engineering design for a facility spanning ~9 hectares with primary product storage in a purpose-built 52-metre diameter dome.

- Storage, handling and dispatch systems for treated silica products.

- Procurement and supply input for major processing equipment.

Taken together, the scope suggests that Homerun is progressing beyond conceptual process design and toward a more detailed understanding of how the facility could ultimately be constructed, equipped, commissioned and operated.

While additional engineering and development work remains ahead, the completion of the CAPEX estimate represents one of the first tangible milestones in translating the company’s silica purification strategy into a defined industrial project with measurable cost, scope and scale.

The strategic role of the facility was emphasized by Homerun‘s COO, Armando Farhate, who stated in today‘s news:

“We are rapidly advancing our silica sand development pathway to primary stage 3N industrial grade silica. It is our plan that this will be one of the highest quality industrial silica sands in Brazil. The output from this primary purification plant will supply our industrial grade customers and our 1,000 tons per day solar glass facility, supporting our vertical integration strategy, and provide clean feed for our 4N and 5N purification processing and advanced materials initiatives in the Silica Valley Industrial Hub.“

Farhate‘s comments reveal the central logic behind Phase 1: The facility is not being developed solely as a processing plant, but as a supply hub intended to serve both external customers and Homerun‘s own downstream manufacturing initiatives, creating an operational link between commercial silica sales, internal manufacturing demand and future downstream expansion opportunities.

This dual-purpose model is important. A plant serving only third-party buyers would primarily be a processing business. A plant serving only internal demand would function largely as a captive feedstock source. Homerun is positioning Phase 1 to do both: Create a commercial outlet for industrial silica sales while simultaneously supplying future value-added manufacturing operations.

Simplicity Matters

In the mining sector, large CAPEX numbers often come with large uncertainty. Many resource projects require complex pre-production buildouts: Mine development, crushing, grinding, flotation, leaching, tailings facilities, water systems, power lines, access roads, camps, port logistics and environmental infrastructure.

Each additional step adds cost. Each added circuit adds technical risk. Each new assumption adds another layer of uncertainty between the feasibility study and real-world execution.

One of the great challenges for investors in mining development stories is that feasibility studies can appear highly precise on paper, yet they remain engineering models built on assumptions about geology, metallurgy, construction costs, recoveries, reagent consumption, operating conditions, timelines and market prices.

In practice, projects can face ore variability, unexpected impurities, harder material than anticipated, lower recoveries, permitting delays, inflation, contractor issues or processing bottlenecks that only become fully visible during construction, commissioning or early operations.

That is why many mining projects move through laboratory testing, bench-scale work and pilot-scale programs before attempting to finance and build a full mine. Even then, translating a study into operating reality can be difficult. A flow sheet that performs well under controlled test conditions may require adjustment once exposed to real-world mining conditions and variable feed material.

Against that backdrop, Homerun‘s Phase 1 silica purification plant stands apart.

The planned facility is not a conventional hard-rock mine concentrator. It is not built around crushing, grinding, flotation, pressure oxidation, cyanidation, solvent extraction or complex metallurgical recovery.

In Homerun’s case, the process route is based on physical purification steps, including washing, grading, sieving, attrition scrubbing, classification and drying. This gives the project a different technical profile: A silica sand purification plant with fewer major processing steps, lower apparent metallurgical complexity and a sub-10 million USD CAPEX may carry a different risk profile than many traditional mining developments.

The process still needs to be engineered, financed, built, commissioned and operated successfully, but the technical pathway appears more straightforward than many complex metals projects where geology and metallurgy can materially change the outcome.

This helps explain why the CAPEX estimate may be more meaningful than it first appears. It is not a large number by mining-sector standards. But that is precisely the point. If Homerun can establish its first commercial purification layer with a comparatively modest capital requirement and a relatively simple physical processing route, the company may be able to reduce the scale of upfront execution risk while creating the foundation for a much larger downstream strategy.

In other words, the Phase 1 plant is small in CAPEX, but potentially large in strategic leverage.

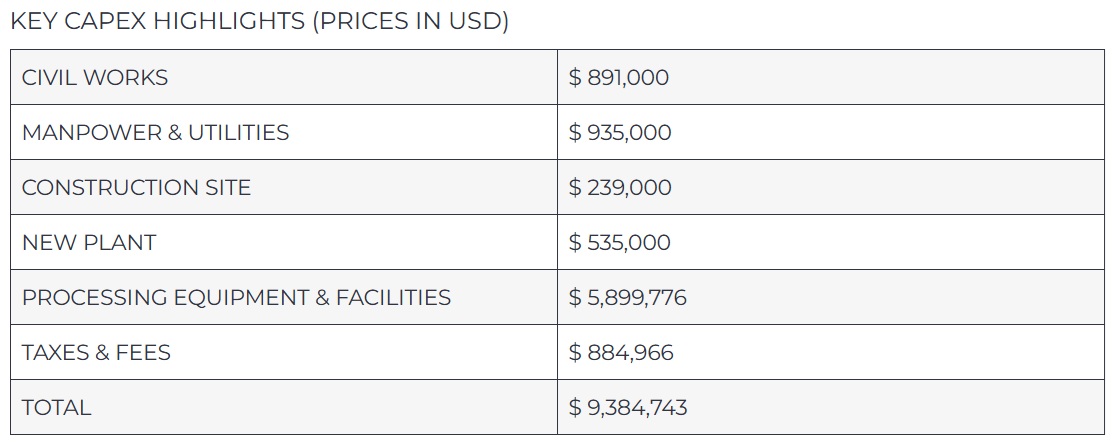

Putting the Numbers Into Perspective

At first glance, the CAPEX estimate of 9.38 million USD may appear surprisingly low for a facility designed to process 350,000 tonnes of silica sand per year.

By mining-sector standards, a sub-10 million USD processing facility is relatively uncommon, particularly for a project intended to become the first industrial layer of a broader value-added manufacturing strategy.

Viewed another way, the estimate equates to ~26.8 USD of capital investment per tonne of annual processing capacity. While capital intensity metrics vary significantly across industries and processing technologies, the figure provides a useful benchmark for investors assessing the scale of the proposed buildout.

Notably, ~63% of the total budget is allocated to processing equipment and facilities, underscoring that the majority of the investment is directed toward the core purification infrastructure rather than ancillary site development.

For a company pursuing a vertically integrated silica strategy, the significance of the expenditure lies less in the absolute CAPEX figure and more in the industrial capability it is intended to create.

Bottom Line

For Homerun, the significance of today‘s announcement is not simply that the company has budgeted a 9.38 million USD silica purification plant. The significance is that the vision of a vertically integrated silica industrial hub is becoming increasingly tangible, moving steadily from concept and engineering studies toward physical industrial development.

Over the past year, Homerun has steadily assembled the building blocks of what it now calls the “Silica Valley of Bahia”: A high-purity silica resource, a planned solar glass manufacturing facility, advanced purification initiatives targeting higher-purity silica products and the industrial infrastructure required to connect them.

The planned Phase 1 purification plant now emerges as the critical first industrial link in that chain. Its importance lies not only in what it produces, but in what it enables. With a comparatively modest capital requirement, a physical purification route and a clear role inside Homerun’s broader industrial buildout, the facility could become the first operational layer of a much larger silica ecosystem.

While every industrial project carries execution risk, Phase 1 stands apart from many mine development projects that depend on complex metallurgy, large-scale mine infrastructure and far higher upfront capital commitments.

That difference is what gives Phase 1 its strategic weight. This is more than a processing plant. It is the point where Santa Maria Eterna begins to move from geology into industry. From raw silica sand to solar glass. From purified feedstock to advanced materials. From resource potential to industrial capacity.

The sand has already been discovered. The next chapter is conversion – and the result is industrialization.

With the completion of the Phase 1 CAPEX estimate, another piece of Homerun‘s transformation has moved from concept toward reality, as the foundations of the “Silica Valley of Bahia“ continue to take shape in Brazil, one engineered step at a time.

Company Details

Homerun Resources Inc.

#2110 – 650 West Georgia Street

Vancouver, BC, V6B 4N7 Canada

Phone: +1 844 727 5631

Email: info@homerunresources.com

www.homerunresources.com

ISIN: CA43758P1080 / CUSIP: 43758P

Shares Issued & Outstanding: 77,333,285

Canada Symbol (TSX.V): HMR

Current Price: 0.79 CAD (06/05/2026)

Market Capitalization: 61 Million CAD

Germany Ticker / WKN: 5ZE / A3CYRW

Current Price: 0.50 EUR (06/08/2026)

Market Capitalization: 39 Million EUR

Stephan Bogner

Contact

Rockstone News & Research

Stephan Bogner (Dipl. Kfm., FH)

Müligässli 1, 8598 Bottighofen

Switzerland

Phone: +41-71-5896911

Email: info@rockstone-news.com

Disclaimer and Information on Forward Looking Statements: Rockstone and Homerun Resources Inc. (“Homerun“) caution investors that any forward-looking information provided herein is not a guarantee of future results or performance, and that actual results may differ materially from those in forward-looking information as a result of various factors. The reader is referred to Homerun’s public filings for a more complete discussion of such risk factors and their potential effects, which may be accessed through its documents filed on SEDAR+ at www.sedarplus.ca. All statements in this report, other than statements of historical fact, should be considered forward-looking statements. Much of this report is comprised of statements of projection, interpretation and strategic analysis. Such statements involve known and unknown risks, uncertainties and other factors that may cause actual results, developments or events to differ materially from those anticipated in these forward-looking statements. There can be no assurance that such statements will prove to be accurate, as actual results and future events could differ materially from those anticipated in such statements. Forward-looking statements in this report include statements, interpretations, conclusions, industrial comparisons, strategic observations, engineering assessments, CAPEX commentary, industrial analogies and market commentary regarding Homerun’s proposed silica purification facility, vertically integrated industrial hub, high-purity silica resources, downstream manufacturing initiatives and broader “Silica Valley of Bahia” strategy. Forward-looking statements include expectations regarding the Company’s planned 350,000 tonne per year (tpy) Phase 1 silica purification facility in Belmonte, Bahia, Brazil, including assumptions related to engineering studies, capital cost estimates, process flow design, throughput capacity, product quality, commissioning, operating performance, storage infrastructure, logistics systems, construction timelines, procurement activities, commercial operations and future integration with downstream manufacturing initiatives. Forward-looking statements further include expectations regarding Homerun’s broader silica purification roadmap, including assumptions that the Company may successfully advance future 4N and 5N purification stages, advanced silica materials initiatives, solar glass feedstock integration and vertically integrated industrial manufacturing operations. Forward-looking statements also include expectations regarding the Company’s proposed solar glass manufacturing facility, including assumptions related to production capacity, antimony-free solar glass production, project economics, NPV, IRR, payback, CAPEX, site layout, future expansion opportunities, customer demand, domestic and export markets, offtake opportunities, financing, construction, commissioning and the facility’s role within the Company’s broader industrial development strategy. Forward-looking statements further include expectations regarding the Company’s advanced materials initiatives, including assumptions related to fused silica, silicon carbide, high-purity silica-derived products, semiconductor-related applications, photonics, power electronics, quartzware, advanced manufacturing applications and ongoing research and development activities. Forward-looking statements also include statements regarding financing discussions, strategic partnerships, infrastructure development, industrial ecosystem formation, customer qualification, manufacturing scale-up, technology deployment and commercialization opportunities. Forward-looking statements are based on current expectations, estimates and assumptions that are inherently subject to uncertainty and may differ materially from actual outcomes. Industrial Hub Development Risks: Statements regarding Homerun’s potential evolution into a vertically integrated silica industrial hub are subject to substantial execution risk. The Company remains in a development-stage phase and may face significant challenges associated with engineering, financing, permitting, procurement, construction, commissioning, manufacturing ramp-up, customer qualification, operational scaling, supply-chain integration and commercial execution. There can be no assurance that Homerun will successfully establish the integrated industrial ecosystem described or implied in this report. Silica Valley Strategy Risks: Statements regarding the development of the “Silica Valley of Bahia” are forward-looking and conceptual in nature. There can be no assurance that Homerun will successfully establish the industrial cluster, attract strategic partners, secure financing, develop supporting infrastructure, achieve commercial scale or realize the integration benefits discussed in this report. Industrial ecosystem development is complex and may be affected by financing constraints, infrastructure limitations, permitting delays, market conditions, partner performance, regulatory developments and broader economic factors. Engineering and CAPEX Estimate Risks: Statements regarding the Phase 1 purification facility CAPEX estimate, engineering studies, process design, equipment specifications, infrastructure requirements, facility footprint, storage systems, construction scope, procurement activities, operating assumptions, commissioning schedules or project development timelines are forward-looking and subject to uncertainty. Preliminary engineering studies and capital cost estimates may change as additional engineering work, procurement activities, permitting requirements, contractor selection, financing activities and project development advance. Actual project costs, schedules, technical specifications and operating outcomes may differ materially from current estimates. Purification Process Risks: Statements regarding washing, grading, sieving, attrition scrubbing, classification, drying, impurity removal, product consistency, silica purity levels, throughput capacity, process performance, operational efficiency or commercial-scale production are subject to technical and operational uncertainty. Laboratory observations, engineering assumptions and pilot-scale results may not translate directly to commercial-scale operations. There can be no assurance that the proposed process route will consistently achieve anticipated product specifications, production volumes, operating efficiencies, purity levels, recovery rates or customer qualification standards. Purity and Product Quality Risks: Statements regarding the production of 3N, 4N or 5N silica products are forward-looking and subject to technical risk. Silica purity, contamination levels, particle-size distribution, product consistency and customer acceptance may vary due to geology, operating conditions, process performance, scale-up challenges, equipment performance, quality-control requirements and customer-specific technical specifications. Industrial Infrastructure Risks: Statements regarding facility layout, storage infrastructure, handling systems, dispatch facilities, logistics systems, utility requirements, the proposed 52-metre storage dome, site footprint or broader industrial infrastructure development are forward-looking and subject to engineering, permitting, financing, procurement, construction and operational risks. There can be no assurance that infrastructure components will be developed according to current plans, budgets, schedules or performance expectations. Solar Glass Development Risks: Statements regarding the proposed solar glass manufacturing facility are forward-looking and subject to significant uncertainty. There can be no assurance that the facility will be financed, constructed, commissioned or operated according to current expectations, or that it will achieve anticipated production capacity, operating performance, customer acceptance, margins, economics, offtake volumes or commercial returns. Advanced Materials Risks: Statements regarding fused silica, silicon carbide, semiconductor-related materials, photonics, quartzware, power electronics, advanced manufacturing applications, 4N or 5N silica products or other high-purity silica-derived materials are inherently speculative and subject to substantial technical and commercial uncertainty. There can be no assurance that development efforts, pilot work, research activities or future production initiatives will result in commercially viable products or market acceptance. Financing Risks: Statements regarding financing discussions, strategic interest, project funding, infrastructure financing, lender engagement or investment participation are inherently forward-looking. There can be no assurance that discussions with strategic investors, lenders, infrastructure partners, development institutions or commercial counterparties will result in financing commitments or funding arrangements on acceptable terms or at all. Construction and Operational Risks: Development of industrial processing, purification and manufacturing facilities involves substantial risks, including engineering challenges, contractor performance issues, cost escalation, permitting delays, commissioning challenges, equipment failures, infrastructure dependencies, workforce limitations, supply-chain disruptions and operational ramp-up risks. There can be no assurance that the Company’s projects will be developed, constructed or operated according to current expectations, budgets or timelines. Comparative Analysis Risks: Statements regarding project simplicity, capital intensity, execution risk, processing complexity, industrial comparisons, mining-sector comparisons, CAPEX benchmarks, strategic leverage, industrial analogies or relative project risk are based on the author’s opinions, assumptions and analytical judgments. Such comparisons are inherently subjective and should not be interpreted as guarantees of project success, financing outcomes, construction performance, operating results, economic returns or commercial viability. Market Demand and Commercialization Risks: Statements regarding industrial silica demand, solar glass demand, advanced materials markets, customer demand, downstream manufacturing opportunities or broader commercialization prospects are subject to market uncertainty. Demand for silica products, advanced materials, solar glass or related industrial products may be affected by market conditions, pricing pressure, competing technologies, customer qualification requirements, regional overcapacity, import competition, regulatory developments and broader economic conditions. Brazil and Jurisdictional Risks: Statements regarding infrastructure development, permitting, industrial policy, regional economic development, government support, financing programs or broader manufacturing initiatives in Brazil are subject to political, regulatory, administrative and economic uncertainty. Government priorities, permitting processes, incentives, tax treatment, infrastructure commitments and policy frameworks may change and may not result in the anticipated benefits. Macroeconomic and External Risks: Homerun’s business and development plans may be affected by broader macroeconomic, geopolitical, regulatory, energy-market, inflationary, currency, commodity-price, supply-chain or capital-market developments. External events including political instability, changes in trade policy, labor shortages, energy-price volatility, financing constraints, infrastructure disruptions or broader economic conditions may materially impact the Company’s development plans, financing prospects, construction timelines or commercial opportunities. Accordingly, readers should not place undue reliance on forward-looking information. Actual results may differ materially from those expressed or implied in the forward-looking statements contained in this report. Rockstone and the author of this report do not undertake any obligation to update any statements made herein except as required by applicable law. Past performance, comparisons to other companies, projects, commodities, technologies, jurisdictions, feasibility studies, capital-market events or industry trends are provided for illustrative purposes only and should not be considered indicative of future results.

Disclosure of Interest and Advisory Cautions: Nothing in this report should be construed as a solicitation to buy or sell any securities mentioned. Rockstone, its owners and the author of this report are not registered broker-dealers or financial advisors. Before investing in any securities, you should consult with your financial advisor and a registered broker-dealer. Never make an investment based solely on what you read in an online or printed report, including Rockstone’s report, especially if the investment involves a small, thinly-traded company that isn’t well known. The author of this report, Stephan Bogner, is paid by Homerun Resources Inc. On September 8, 2025, Homerun announced that the company “entered into an agreement with Rockstone Research to provide marketing services to the company”, and that “Rockstone Research is an arm’s-length marketing firm and has been engaged for an initial three-month term for total consideration of $25,000, which is payable up front. The company does not propose to issue any securities to Rockstone in consideration for the services to be provided to the company.” The marketing services agreement has since been extended and remains in effect as of the date of this report. The author owns equity of Homerun and thus will profit from volume and price appreciation of the stock. This also represents a significant conflict of interest that may affect the objectivity of this reporting. The author may buy or sell securities of Homerun (or comparable companies) at any time without notice, which may give rise to additional conflicts of interest. Overall, multiple conflicts of interests exist. Therefore, the information provided in this report should not be construed as a financial analysis or recommendation but as an advertisement. This report should be understood as a promotional publication and does not replace individual investment advice. Rockstone’s and the author’s views and opinions regarding the companies that are featured in the reports are the author‘s own views and are based on information that was received or found in the public domain, which is assumed to be reliable. Rockstone and the author have not undertaken independent due diligence of the information received or found in the public domain. Rockstone and the author of this report do not guarantee the accuracy, completeness, or usefulness of any content of this report, nor its fitness for any particular purpose. Lastly, Rockstone and the author do not guarantee that any of the companies mentioned in the reports will perform as expected, and any comparisons that were made to other companies may not be valid or come into effect. For the avoidance of doubt, this report is not intended for distribution to, or use by, any person or entity in any jurisdiction where such distribution, publication or use would be contrary to local law or regulation. Readers are solely responsible for ensuring that their review and use of this report is lawful in their jurisdiction. Neither Rockstone nor the author accepts liability for any direct or indirect loss arising from the use of this report or from any investment decision made in reliance on it. Please read the entire Disclaimer carefully. If you do not agree to all of the Disclaimer, do not access this website or any of its pages including this report in form of a PDF. By using this website and/or report, and whether or not you actually read the Disclaimer, you are deemed to have accepted it. Information provided is educational and general in nature and should not be interpreted as personalized investment, financial, legal, tax or professional advice. Data, tables, figures and pictures, if not labeled or hyperlinked otherwise, have been obtained from Stockwatch.com, Tradingview.com, Homerun Resources Inc. and the public domain.