This week’s announcement of the completed Bankable Feasibility Study (BFS) was not only transformational for Homerun Resources Inc. as a company. It was also transformational for shareholders trying to understand what they are actually dealing with here, and why the story may be broader than mining.

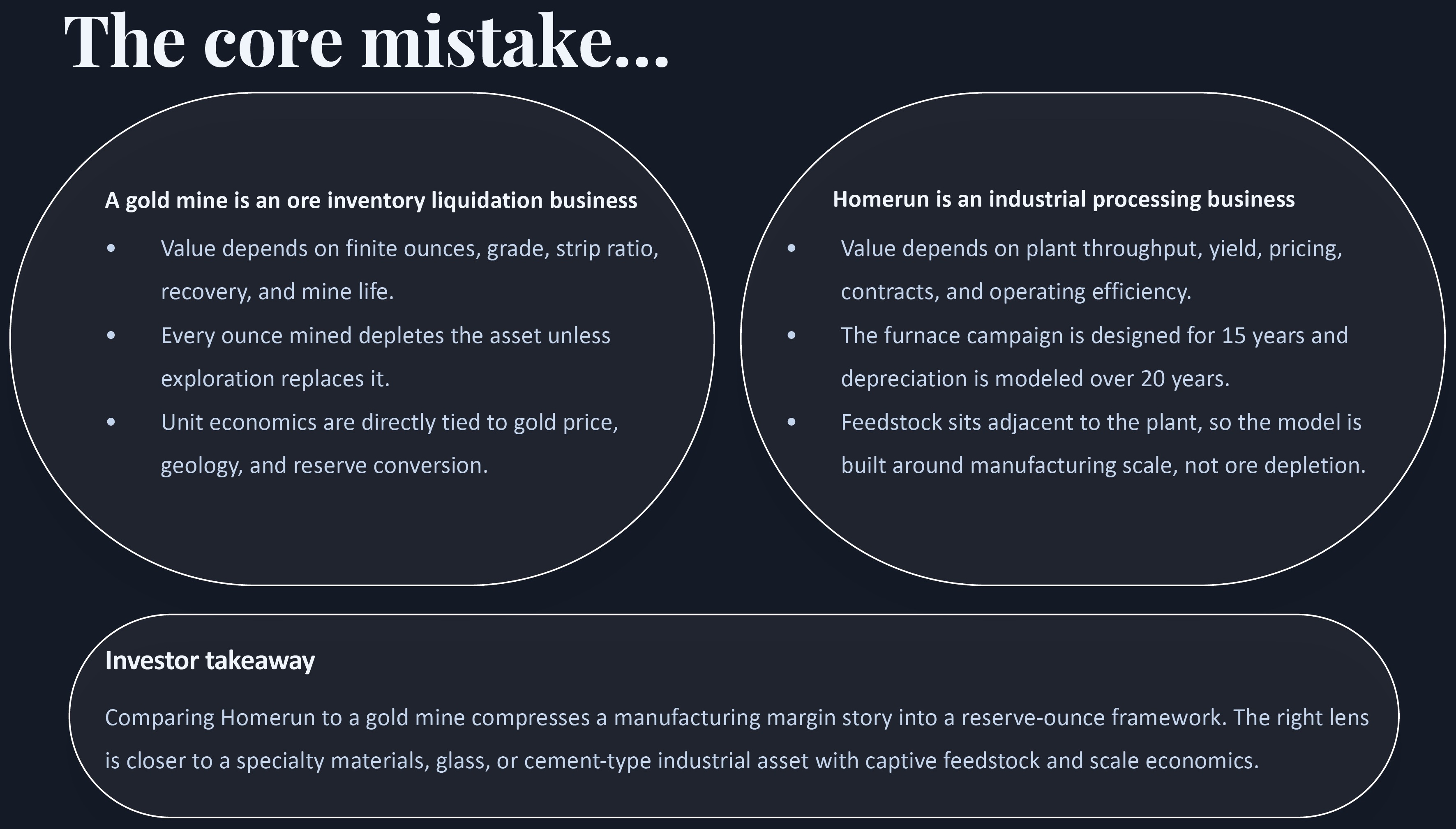

This report raises an important question that many resource investors are still struggling with: If a solar glass manufacturing plant has an expected operating life of roughly 15 years before refurbishment, how is that fundamentally different from a mine with a finite reserve life? At first glance, the comparison appears logical.

A gold mine has a mine life.

A solar glass plant has a furnace campaign life.

Both eventually require large capital expenditures. Both depreciate over time. And both can look deceptively similar on paper.

So why do industrial platform companies often command materially stronger market premiums than mining companies?

The answer lies in the difference between:

- Depleting vs renewable assets

- Extraction vs value-added manufacturing

- Geological uncertainty vs engineered production

- One-time resource monetization vs recurring industrial cash flow

- Cyclical speculation vs strategic infrastructure positioning

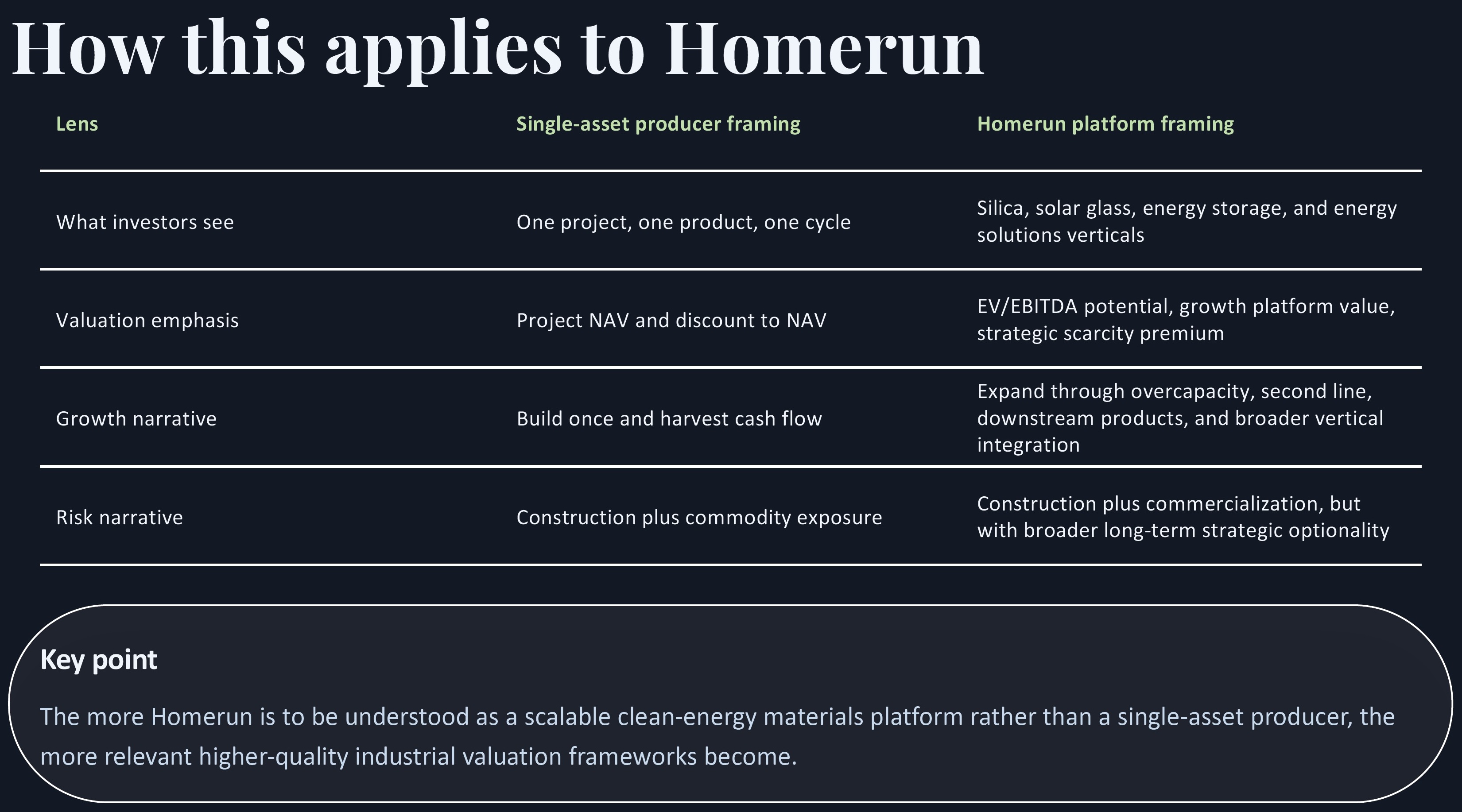

This distinction is at the heart of why Homerun may increasingly be viewed less like a junior mining company and more like an infrastructure-linked industrial platform.

That shift in perception may ultimately become the central investment debate.

The Opportunity

Despite the company’s positioning around ultra-high purity silica sand and solar glass infrastructure, a significant portion of the market still appears to benchmark Homerun using traditional mining metrics:

- Resource size

- Grade

- Exploration upside

- Future production assumptions

- Permitting risk

- Capex intensity

- Commodity exposure

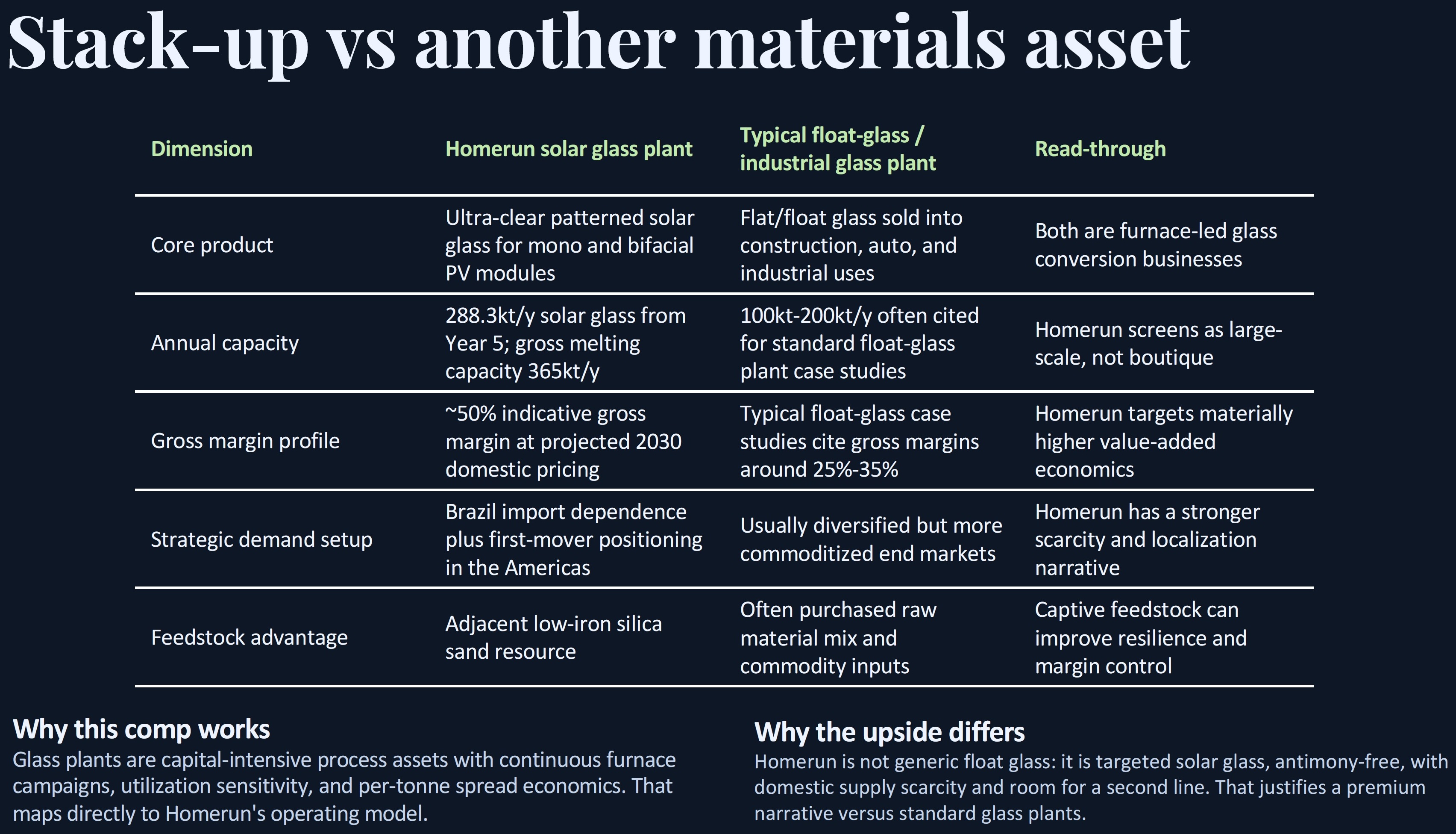

That framework may no longer be sufficient. The visuals presented in this report points to a much broader ambition: Not only supplying silica sand, but vertically integrating into the downstream solar glass value chain.

This matters because downstream manufacturing economics are fundamentally different from upstream extraction economics. At projected full-rate production, this is not a small resource processing concept. The BFS model point to annual revenue of ~344.9 million USD, driven by tonnes of finished solar glass rather than ounces, grade or reserve conversion. That scale matters because it reinforces the central point: Homerun is not simply attempting to monetize a silica deposit, but to convert that feedstock into a higher-value manufactured product with industrial revenue potential.

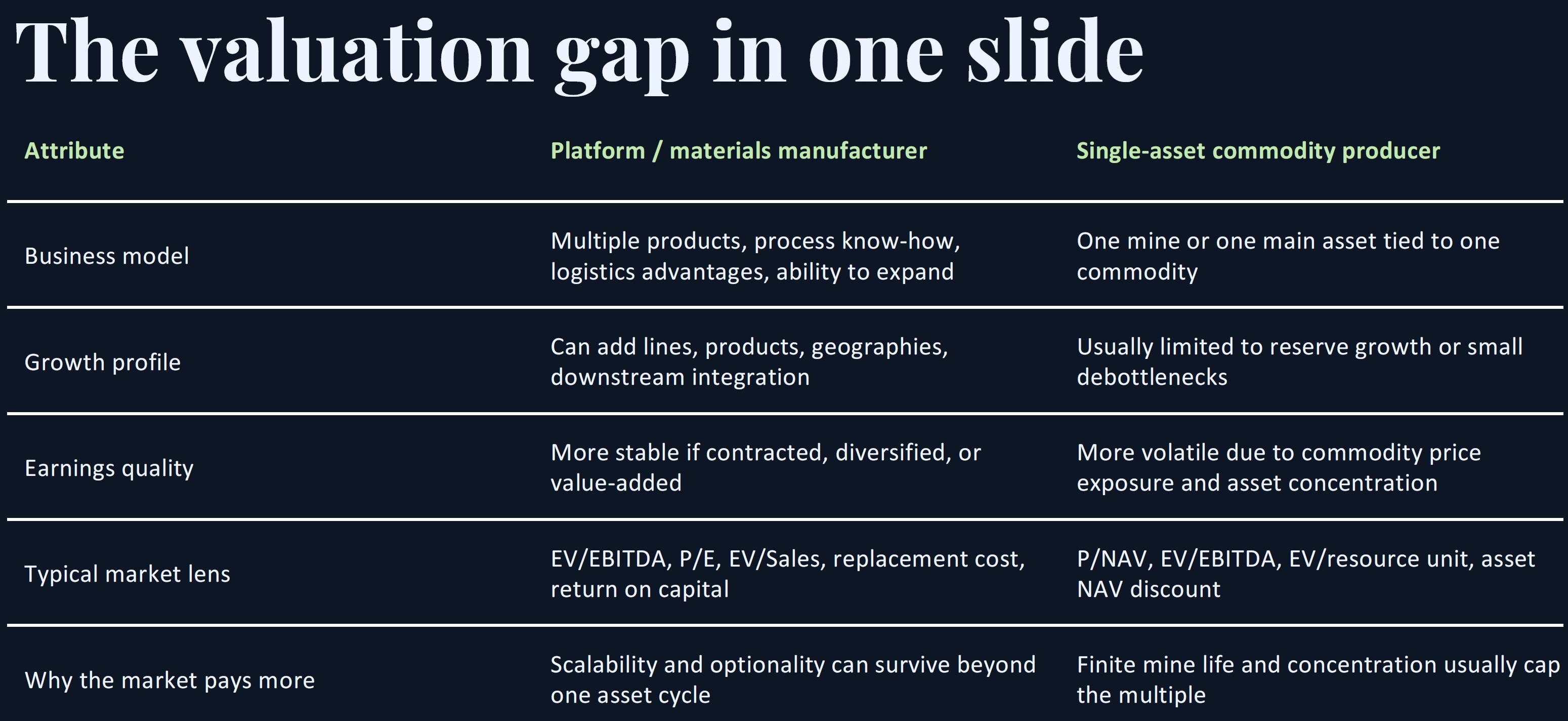

A mine extracts value from a finite deposit. An industrial platform can continue generating value indefinitely, provided it remains technologically and economically competitive.

That distinction is critical.

A Mine is Consumed – A Factory is Maintained

This is perhaps the simplest and most important conceptual difference: A mine is depleted. Every tonne extracted permanently reduces the remaining asset base. Eventually:

- Ore grades decline

- Strip ratios rise

- Costs increase

- Reserves diminish

- Closure approaches

In many cases, the asset literally disappears economically.

A solar glass plant works differently. The furnace itself has a campaign life, often around 12-15 years before major rebuild. But the plant does not disappear. The site remains. The infrastructure remains. The customer relationships remain. The logistics remain. The permits remain. The industrial ecosystem remains.

The furnace rebuild is not analogous to exhausting an orebody. It is more comparable to replacing a jet engine on an aircraft or overhauling a blast furnace in steel production. Industrial facilities routinely undergo:

- Furnace rebuilds

- Efficiency upgrades

- Automation modernization

- Capacity expansions

- Fuel system conversion

- Digital optimization

These are lifecycle investments, not terminal events. This is why industrial assets are often modeled similarly to infrastructure assets.

15 Years is Not the End Date

One of the biggest misconceptions among mining investors entering industrial manufacturing analysis is assuming that a furnace campaign life defines the life of the business. It does not.

Glass manufacturing furnaces are designed around campaign cycles. After approximately 12-15 years:

- Refractory materials degrade

- Efficiency declines

- Thermal stress accumulates

- Maintenance costs increase

At that point, operators typically shut down the furnace temporarily and rebuild or reline it. But critically:

- The factory continues existing

- The industrial footprint remains valuable

- Production resumes afterward

- The customer base often remains intact

- The surrounding infrastructure retains value

Some glass manufacturing sites have operated continuously for multiple decades, even generations. The furnace campaign is therefore closer to a major maintenance cycle than a mine closure. This is an enormous conceptual distinction.

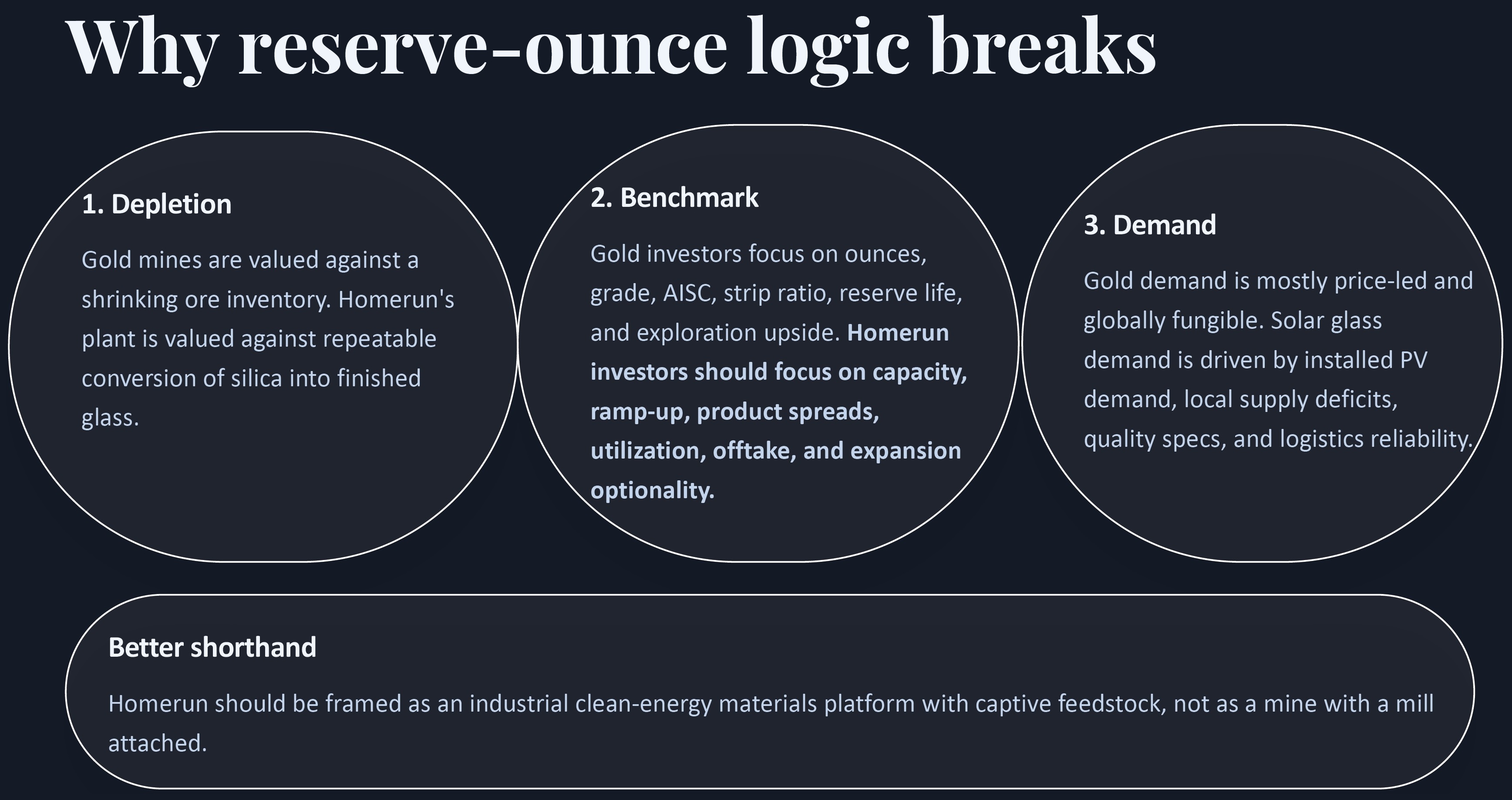

Mining investors often focus on depletion curves. Industrial investors focus on operating continuity.

Platforms Command Premiums

Mining companies often trade at lower valuation multiples because investors know the assets are wasting assets. The reserve base is continuously shrinking.

Even highly profitable mines face a constant replacement problem: They must continuously discover or acquire new deposits just to sustain long-term production. This creates:

- Exploration risk

- Reserve replacement risk

- Permitting uncertainty

- Geopolitical exposure

- Declining grade risk

- Operational variability

Industrial manufacturing assets, especially strategic infrastructure assets, are valued differently.

Why? Because investors prioritize:

- Durability of cash flow

- Customer stickiness

- Strategic positioning

- Barriers to entry

- Replacement cost

- Recurring demand

- Scalability

This is where the Homerun thesis becomes more interesting: The company is not only talking about selling sand. It is positioning itself around participation in a supply-chain-critical industrial bottleneck. That changes the market’s perception.

One reason this distinction matters is that capital markets tend to reward durability and scalability more than finite extraction.

A mine, no matter how profitable, is constantly fighting depletion. Investors know the asset base shrinks every day production continues. The business therefore requires continuous replacement through exploration success, acquisitions or reserve expansion simply to maintain long-term relevance.

Industrial manufacturing platforms operate differently. Once core infrastructure, customer relationships, logistics networks and operational expertise are established, growth can increasingly come from optimization and expansion rather than from discovering entirely new deposits. That creates a fundamentally different long-term profile.

Additional production may come from:

- Debottlenecking

- Process optimization

- Second production lines (Phase 2)

- Downstream integration

- Adjacent product categories

- Geographic expansion

In other words, the value creation pathway becomes industrial scaling rather than geological replacement.

That is a major reason why certain industrial materials businesses often command stronger market confidence than traditional extractive industries, even when both require significant upfront capital investment.

Solar Glass: Not a Typical Commodity Business

Many investors underestimate how strategically important solar glass has become. Solar panels cannot exist without specialized glass. And not all glass qualifies. Solar glass requires:

- Very high optical transmission

- Extremely low iron content

- Thermal durability

- Manufacturing precision

- Large-scale industrial consistency

The global solar industry is rapidly expanding, yet solar glass manufacturing capacity outside China remains relatively limited.

This creates an unusual dynamic: The bottleneck is not only the raw silica. The bottleneck is downstream conversion capacity. That distinction matters enormously.

This is where many mining investors may still underestimate the strategic importance of what Homerun is building: Ultra-high purity silica alone is not the scarce asset. The real scarcity increasingly lies in industrial conversion infrastructure capable of reliably producing solar-grade glass at scale.

In other words, the challenge is no longer simply digging material out of the ground. The challenge is building localized industrial ecosystems capable of supplying the global solar buildout with dependable, high-volume, specification-grade materials.

That is why governments, manufacturers and supply chains increasingly focus on downstream processing capacity rather than raw resource ownership alone. Industrial conversion capability can become strategically more valuable than the underlying feedstock itself.

Owning high-purity silica resources alone may not justify premium valuations. Owning strategic downstream processing capacity potentially can. Especially if:

- Regional supply chains localize

- Trade restrictions increase

- Governments subsidize domestic production

- Energy transition infrastructure accelerates

- Manufacturers seek non-Chinese supply chains

The market may therefore begin treating certain solar glass assets more like essential infrastructure than cyclical commodity operations.

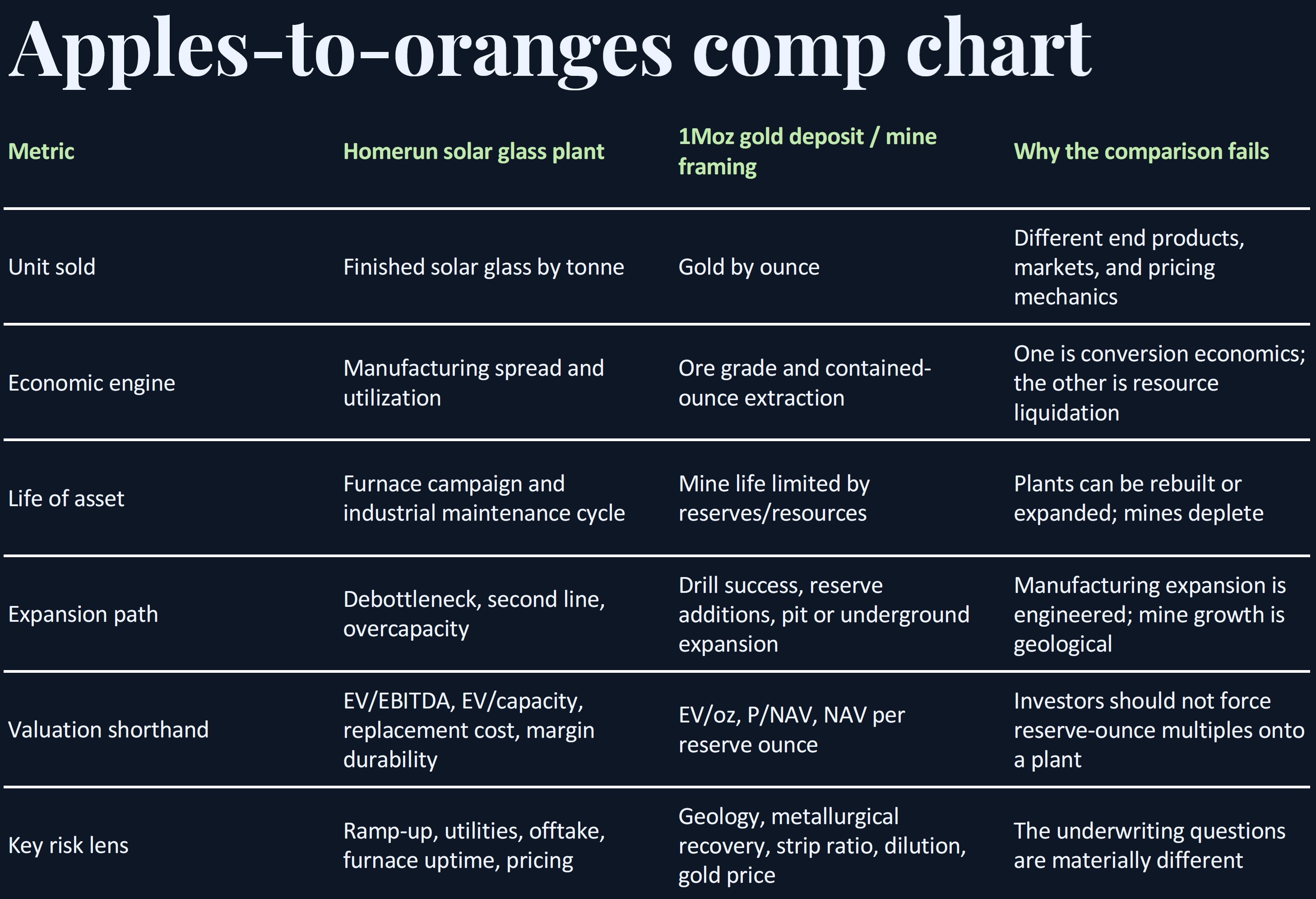

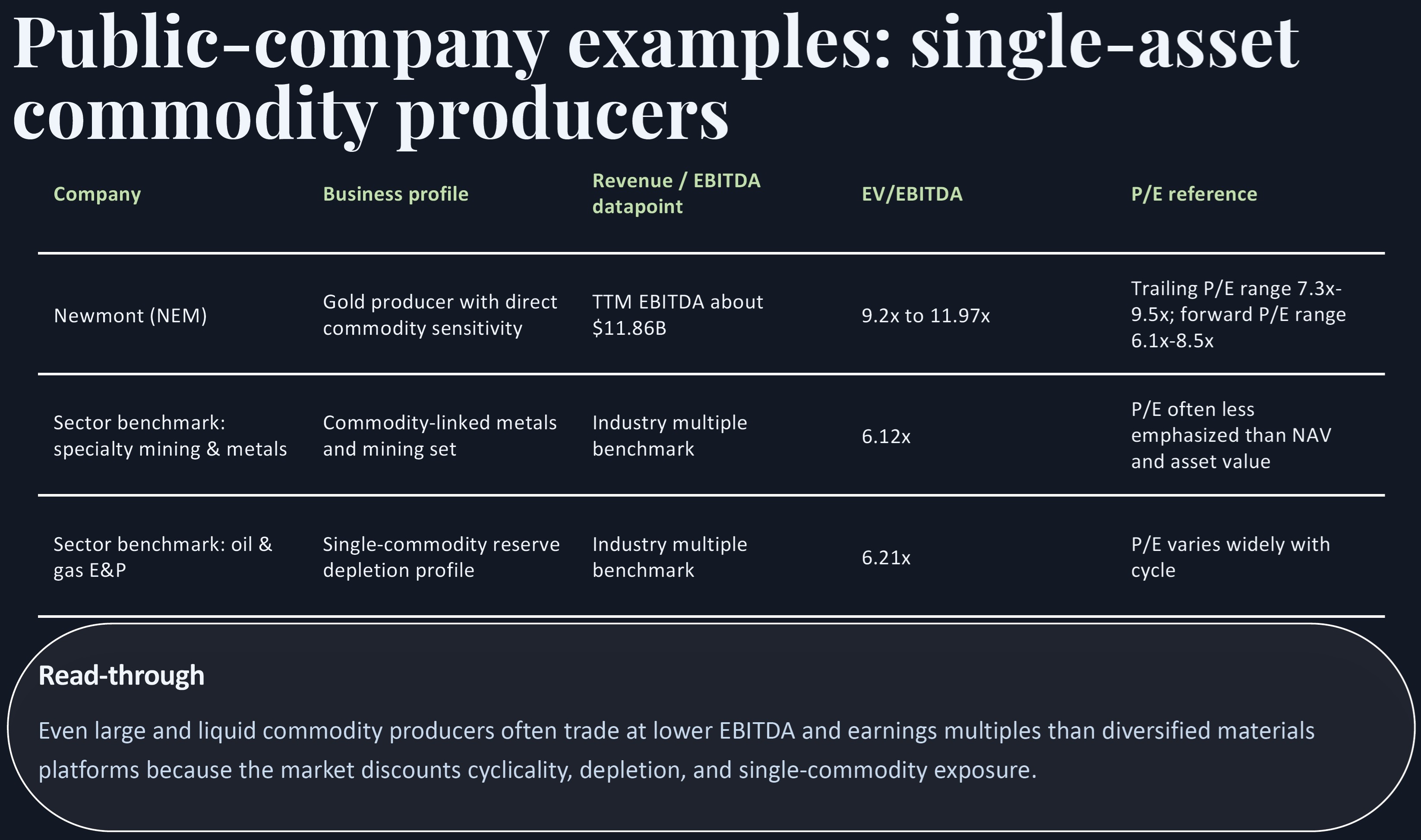

The Comparison to Gold Mining Breaks Down Quickly

The gold mining analogy helps illustrate why the valuation gap exists. A gold producer typically faces:

- Declining reserves

- Uncertain exploration success

- Exposure to ore variability

- Volatile sustaining costs

- Uncertainty around long-term reserves

- Jurisdictional risk

- Limited pricing power

Meanwhile, a strategically positioned solar glass platform may benefit from:

- Long-term contracted demand

- Recurring industrial customers

- Recurring manufacturing margins

- Scalable production systems

- Technological optimization

- Integration into energy infrastructure

- Policy support from governments

Most importantly: The industrial asset can continue operating long after the initial furnace campaign. A mine eventually disappears. A factory can theoretically operate indefinitely.

That difference alone changes how investors model terminal value.

Maintenance, Not Mine Closure

This does not mean furnace rebuilds are insignificant. They absolutely matter. A furnace rebuild is capital intensive. Investors should not ignore:

- Future rebuild costs

- Downtime during refurbishment

- Financing requirements

- Technological obsolescence risk

- Energy cost competitiveness

Importantly, this becomes even more relevant if Homerun eventually develops a second production line (Phase 2). While Phase 2 is not part of the current BFS scope, the Company has referenced a potential second 1,000 tpd line that could lift combined annual production to ~576,600 tpy, effectively doubling full-rate capacity from Phase 1. In that scenario, maintenance on the initial line would not necessarily mean a full plant shutdown. One line could be offline for furnace rebuild or major maintenance while the second line continues operating, potentially at high utilization. That is another reason why a multi-line industrial platform should not be viewed the same way as a single finite mine approaching depletion.

However, industrial markets already understand and price these realities. Steel mills, cement plants, chemical facilities, refineries and glass manufacturers all require periodic major maintenance and modernization.

Yet these industries are still valued on ongoing earnings power because the underlying business platform survives beyond any single operating cycle. This is fundamentally different from extracting the last economically recoverable ounce from a deposit.

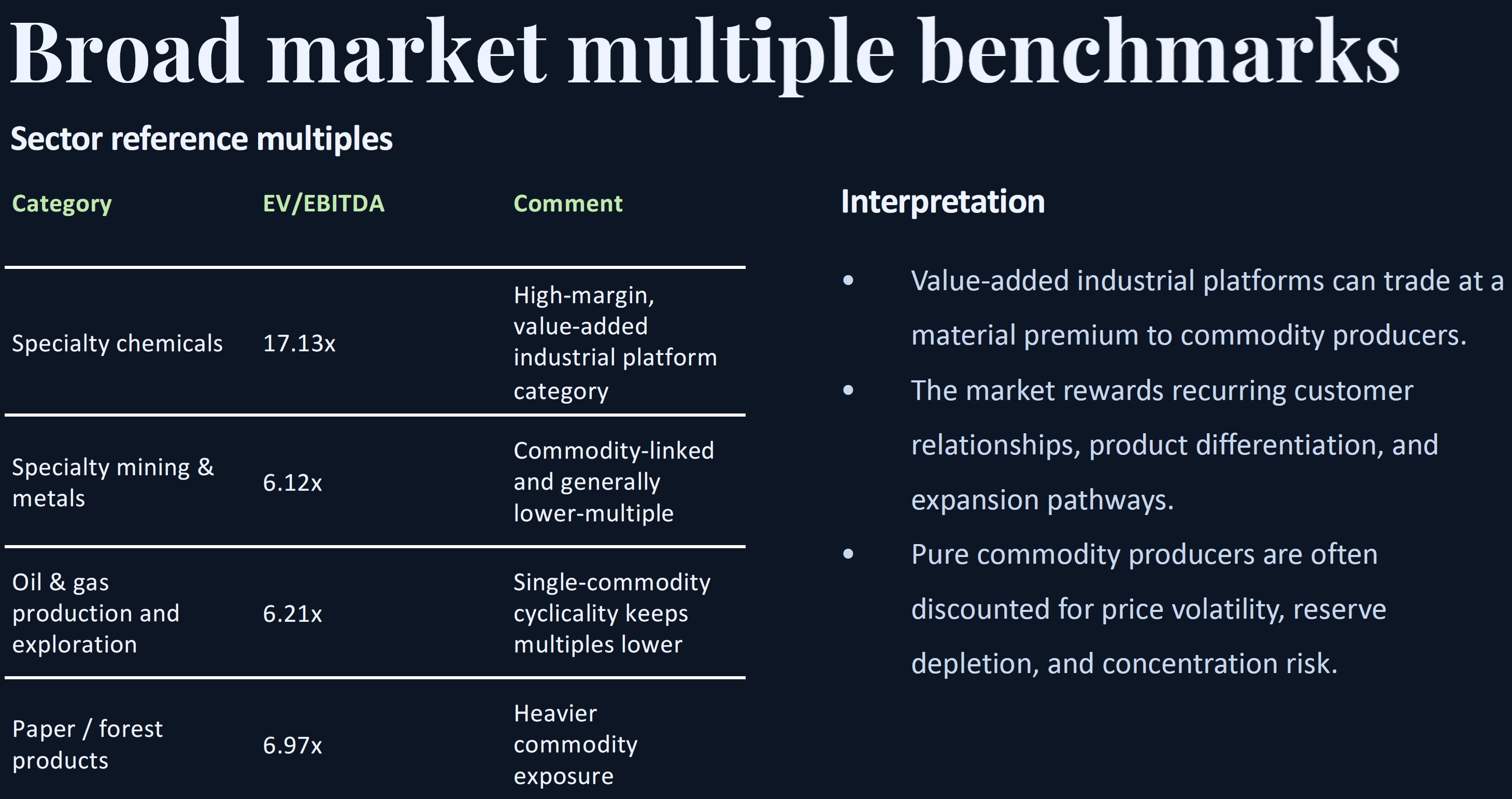

The Drivers Behind the Premium

The higher valuation multiples often seen in industrial platform businesses come from several overlapping characteristics:

1) Replacement Cost Economics

Building new solar glass capacity is expensive and technically difficult. This creates barriers to entry. Once operational, existing facilities become strategically valuable because replicating them requires:

- Enormous capital

- Engineering expertise

- Permitting

- Energy infrastructure

- Logistics integration

- Customer qualification

- Years of development time

This often supports premium valuations.

2) Supply Chain Strategic Importance

Global energy policies increasingly prioritize domestic manufacturing capacity. Countries do not only want raw materials. They want industrial self-sufficiency. This elevates the strategic value of downstream processing infrastructure. Especially in:

- Solar supply chains

- Battery materials

- Semiconductors

- Rare earth processing

- Critical minerals refining

The market may therefore value certain industrial assets more like high-value national infrastructure.

3) Recurring Industrial Demand

Gold demand fluctuates. Exploration cycles fluctuate. Commodity cycles fluctuate. But solar deployment is increasingly tied to structural trends toward energy independence. If solar adoption continues expanding globally, solar glass demand may become more infrastructure-like than cyclical. That creates:

- Longer visibility

- Recurring customer relationships

- Potentially more stable utilization

- Stronger financing conditions

4) Platform Optionality

A vertically integrated industrial platform may expand into:

- Coated glass

- Specialty glass

- Energy storage materials

- Downstream fabrication

- Recycling

- Regional manufacturing hubs

This optionality rarely exists in the same way for a single-asset mining operation.

The Homerun Angle

Investors still appear to view Homerun primarily as a resource company, while the accompanying visuals increasingly point to a broader story:

- Industrial integration

- Downstream manufacturing

- Platform economics

- Infrastructure positioning

- Strategic partnerships

- Value-added conversion

That distinction matters. Exploration companies, mining producers, specialty materials companies, industrial technology platforms and infrastructure-linked manufacturers are not judged through the same lens.

Markets apply very different standards depending on how a company is categorized. Resource companies are often judged on depletion, reserve replacement and commodity exposure. Industrial platform businesses, meanwhile, are more commonly assessed on scalability, recurring demand, operating leverage and strategic positioning within larger supply chains.

This classification lag is common when companies transition from resource development toward downstream industrial manufacturing. Markets often continue applying legacy valuation frameworks long after a company’s strategic direction has evolved, particularly during the development stage when construction, financing and commercialization risks still dominate investor attention. In Homerun’s case, many investors may still primarily associate the company with silica extraction because the industrial platform itself has not yet been fully constructed or demonstrated at commercial scale.

However, capital markets often begin to reassess a business once financing for construction is secured, because that is when a development-stage concept starts moving toward executable industrial reality. The important distinction is that the value proposition increasingly shifts from ownership of a mineral deposit toward ownership of a scalable conversion platform positioned inside a strategically important solar manufacturing supply chain.

This perception gap can materially influence how investors interpret long-term growth potential, durability of earnings and future expansion opportunities.

The opportunity: Homerun may still be widely understood as a silica resource story, while its larger potential lies in becoming a strategic solar infrastructure platform. As that difference becomes clearer, the market’s perception of the company could change substantially.

If Homerun executes, the impact could be significant because investors may begin seeing the business less as finite extraction and more as recurring industrial earnings power.

Bottom Line

The key question is: Can the industrial platform surrounding the plant continue generating economic value over multiple operating cycles?

If the answer is yes, then the comparison to a depleting mine becomes increasingly weak. A mine monetizes a finite geological inventory. A strategically positioned industrial ecosystem monetizes:

- Manufacturing capability

- Customer relationships

- Infrastructure positioning

- Supply chain integration

- Technological know-how

- Industrial scarcity

These are not exhausted by production; they can strengthen as the platform scales, customers are qualified and operating experience accumulates.

That is why industrial infrastructure businesses often command higher valuation multiples than resource extraction ventures. The furnace may eventually need replacement. But replacing a furnace is not the same as replacing a depleted orebody. One is industrial maintenance within an operating ecosystem. The other requires discovering an entirely new economic deposit.

That difference may ultimately define how Homerun is understood over time: Not as a company extracting a finite resource, but as a company establishing long-life industrial infrastructure positioned within one of the world’s fastest-growing manufacturing supply chains.

And that may ultimately become the defining difference between viewing Homerun as a mining story or as an emerging industrial platform.

Company Details

Homerun Resources Inc.

#2110 – 650 West Georgia Street

Vancouver, BC, V6B 4N7 Canada

Phone: +1 844 727 5631

Email: info@homerunresources.com

www.homerunresources.com

ISIN: CA43758P1080 / CUSIP: 43758P

Shares Issued & Outstanding: 77,086,618

Canada Symbol (TSX.V): HMR

Current Price: 0.90 CAD (05/14/2026)

Market Capitalization: 69 Million CAD

Germany Ticker / WKN: 5ZE / A3CYRW

Current Price: 0.555 EUR (05/14/2026)

Market Capitalization: 43 Million EUR

Stephan Bogner

Contact

Rockstone News & Research

Stephan Bogner (Dipl. Kfm., FH)

Müligässli 1, 8598 Bottighofen

Switzerland

Phone: +41-71-5896911

Email: info@rockstone-news.com

Disclaimer and Information on Forward Looking Statements: Rockstone and Homerun Resources Inc. (“Homerun“) caution investors that any forward-looking information provided herein is not a guarantee of future results or performance, and that actual results may differ materially from those in forward-looking information as a result of various factors. The reader is referred to Homerun’s public filings for a more complete discussion of such risk factors and their potential effects, which may be accessed through its documents filed on SEDAR+ at www.sedarplus.ca. All statements in this report, other than statements of historical fact, should be considered forward-looking statements. Much of this report is comprised of statements of projection. Such statements involve known and unknown risks, uncertainties and other factors that may cause actual results or events to differ materially from those anticipated in these forward-looking statements. There can be no assurance that such statements will prove to be accurate, as actual results and future events could differ materially from those anticipated in such statements. Forward-looking statements in this report include statements, interpretations, comparisons, conclusions, graphics, valuation frameworks, industrial analogies, operating-model comparisons, benchmark analyses, multiple comparisons, investor takeaways, strategic interpretations and market observations contained in the embedded presentation slides and visual materials throughout this report, including but not limited to statements regarding Homerun’s positioning as an industrial platform, specialty materials company, infrastructure-linked manufacturing platform or clean-energy materials platform rather than a traditional depleting mining asset. Such statements reflect opinions, interpretations, assumptions and analytical frameworks only and should not be interpreted as guarantees of future valuation outcomes, market recognition, financing success, operating performance or shareholder returns. Forward-looking statements in this report also include expectations related to the commercial, strategic, financial and market implications of Homerun’s completed Bankable Feasibility Study (“BFS”) for its proposed antimony-free solar glass manufacturing facility in Bahia, Brazil, including assumptions that the BFS may support project financing discussions, strategic partnership opportunities, offtake negotiations, permitting activities, construction planning and the Company’s transition into the next phase of development. Forward-looking statements also include expectations regarding the interpretation and potential impact of the BFS results, including assumptions that the reported project economics, including NPV, IRR, CAPEX, OPEX, gross margin, payback period, production capacity, ramp-up profile, sensitivity cases and other financial or technical metrics, may provide a useful basis for evaluating the project’s potential viability, bankability, strategic relevance and possible attractiveness to financing partners, strategic investors and future commercial counterparties. Forward-looking statements further include expectations regarding project financing, including assumptions that discussions with prospective financing partners, state-linked financing sources, development banks, infrastructure investors, strategic partners or other funding sources may progress, that indicative interest may translate into structured financing arrangements and that the Company may secure sufficient capital on acceptable terms to support detailed engineering, project development, construction and initial operations. Additional forward-looking statements include expectations related to the Company’s Sponsored Brazilian Depositary Receipt (“BDR”) program and listing on the B3 stock exchange, including assumptions that the listing may broaden and diversify the shareholder base, may facilitate increased participation from Brazilian institutional investors, family offices, high-net-worth individuals and other qualified investors and may improve the Company’s visibility in the country where its core operations and growth projects are located. Forward-looking statements also include expectations regarding the potential market impact of the BDR structure, including assumptions that demand for BDRs may lead to the acquisition and custody of underlying shares from the TSX Venture Exchange in Canada, may influence trading dynamics and may affect liquidity, float, valuation, arbitrage activity and price discovery over time. Forward-looking statements further include expectations regarding market positioning and industry relevance, including assumptions that Homerun’s high-purity low-iron silica, antimony-free solar glass strategy and vertically integrated platform may align with increasing demand for solar materials, advanced glass, domestic manufacturing, energy infrastructure and supply-chain resilience and may support long-term commercial opportunities across multiple segments of the energy transition. Additional forward-looking statements relate to the Company’s broader platform strategy, including assumptions that Homerun may advance its 4 core verticals, Silica, Solar, Energy Storage and Energy Solutions, and that its silica resource in Bahia may support downstream processing, solar glass manufacturing, advanced materials, long-duration energy storage applications, laser-based purification technologies and related energy applications over time. Forward-looking statements are also made with respect to execution, development and scaling, including assumptions that the Company may successfully advance from feasibility to financing, from financing to construction and from construction to commercial operations, and that timelines, costs, operating parameters, product specifications, customer demand, infrastructure access and ramp-up assumptions may remain within expected ranges. Forward-looking statements also include expectations related to Phase 2 expansion potential, including assumptions that the site may support a second 1,000 tonne per day production line, that shared infrastructure may improve future capital efficiency, that demand may support additional capacity and that any future expansion may create additional value beyond the current BFS scope. Forward-looking statements are based on current expectations, estimates and assumptions that are inherently subject to uncertainty and may differ materially from actual outcomes. Forward-looking statements are subject to risks and uncertainties including, but not limited to: Platform Valuation & Market Re-Rating Risks: Statements regarding potential valuation re-rating, premium industrial multiples, infrastructure-style valuation frameworks, specialty-materials comparisons, EV/EBITDA benchmarks, replacement-cost frameworks, platform economics, scalability narratives, strategic scarcity premiums, recurring earnings assumptions or comparisons to industrial manufacturing businesses are inherently speculative and forward-looking. There can be no assurance that the market will value Homerun as an industrial platform, specialty materials company, infrastructure-linked manufacturing business or vertically integrated clean-energy materials platform rather than as a resource or development-stage company. Market participants may continue applying traditional mining, development-stage, commodity or small-cap valuation methodologies regardless of the Company’s strategic positioning, operational progress or downstream ambitions. Comparisons to specialty chemicals, industrial glass manufacturers, construction materials companies, diversified materials platforms or other industrial businesses may not prove relevant, appropriate or predictive of future valuation outcomes. Industrial Platform Execution Risks: Statements regarding Homerun’s potential evolution into an industrial platform, vertically integrated manufacturing company, specialty materials platform, downstream processing company or broader clean-energy infrastructure participant are subject to significant execution risk. The Company remains in a development-stage phase and may face substantial challenges associated with financing, engineering, construction, commissioning, commercialization, customer qualification, manufacturing ramp-up, operating continuity, industrial process optimization, workforce development, supply-chain integration, downstream product acceptance and long-term competitive positioning. There can be no assurance that Homerun will successfully transition from a resource-development company into a sustainable industrial manufacturing platform or that any anticipated industrial-scale operating advantages, scalability benefits, customer relationships, recurring cash flow characteristics or infrastructure-style valuation attributes will materialize. Comparative Industrial Analogy & Benchmark Risks: References throughout this report and the accompanying presentation materials to gold mines, industrial glass manufacturers, cement plants, float-glass plants, specialty materials companies, construction-materials platforms, industrial infrastructure assets, specialty chemicals companies, mining producers or other analog businesses are provided solely for conceptual illustration and discussion purposes. Such comparisons are inherently imperfect and may not accurately reflect Homerun’s future operating profile, market positioning, financial characteristics, risk profile, capital intensity, customer concentration, competitive environment, regulatory exposure or valuation outcomes. Industrial manufacturing businesses, solar glass facilities, mining projects and vertically integrated materials companies differ materially in operational structure, revenue visibility, replacement economics, financing requirements, scalability, maintenance cycles, cyclicality and long-term risk exposure. Readers should not assume that Homerun will achieve comparable economics, operating metrics, margins, utilization rates, market share, valuation multiples or strategic importance merely because similarities or analogies are discussed in this report or in the embedded presentation materials. Manufacturing Scalability & Expansion Risks: Statements regarding debottlenecking, overcapacity utilization, second production lines, downstream integration, geographic expansion, adjacent product categories, manufacturing scalability, platform optionality, expansion economics, repeatability of industrial capacity or future growth pathways are forward-looking and subject to substantial uncertainty. There can be no assurance that future expansion phases, second-line development, downstream product initiatives, coated glass opportunities, specialty-glass initiatives, energy-storage materials opportunities, regional manufacturing hubs or other industrial expansion concepts will be financed, approved, technically feasible, commercially viable or economically attractive. Expansion opportunities may require substantial additional capital, permitting, customer qualification, utility access, infrastructure upgrades, technology validation and market demand that may not materialize as expected. BFS Interpretation & Model Assumption Risks: Risks that the BFS, while completed, may rely on assumptions, estimates, forecasts, vendor quotations, technical inputs, market data, inflation assumptions, operating-cost assumptions, pricing assumptions, taxation assumptions, discount-rate assumptions or sensitivity cases that may prove inaccurate, incomplete or subject to material revision over time. Financing Risks: Risks that project financing may not be secured on acceptable terms or within expected timeframes, that state-driven, development-bank, infrastructure, strategic or private financing sources may not provide binding commitments, that indicative interest may not convert into executable funding arrangements or that financing conditions may change due to market, macroeconomic, political or project-specific factors. Public-Sector & Development Financing Caution: Statements regarding potential state-linked, development-bank, infrastructure, public-sector-supported or strategic financing are forward-looking and subject to significant uncertainty. There can be no assurance that any government-related or development-finance institution will provide funding, guarantees, incentives, infrastructure support, concessional terms or any other form of financial assistance, or that any such support would be available on terms acceptable to the Company. Construction & Development Risks: Risks associated with advancing from feasibility to construction, including engineering challenges, cost overruns, contractor performance, equipment availability, permitting delays, weather-related delays, infrastructure limitations, local-service constraints, procurement delays and execution risks typical of large-scale industrial manufacturing projects. Permitting & Regulatory Risks: Risks related to environmental approvals, land use, industrial permitting, mining regulations, installation approvals, operating licenses, export controls, taxation, customs duties, local incentives, regulatory interpretation or other legal requirements in Brazil or other relevant jurisdictions. Offtake & Customer Commitment Risks: Risks that existing letters of intent, demand indications, advanced discussions or non-binding commercial expressions may not convert into definitive binding supply agreements, may be delayed, may be renegotiated on less favorable terms or may not generate the expected level of revenue, pricing visibility or bankability support. Market Demand & Industry Risks: Risks that demand for solar glass, photovoltaic modules, high-purity silica or related materials may develop more slowly than expected, may be impacted by changes in solar deployment trends, interest rates, policy frameworks, subsidies, competing technologies, import dynamics or regional imbalances and may be subject to cyclical or structural market changes. Pricing & Margin Risks: Risks that projected domestic selling prices, export pricing, product premiums, inflation assumptions or gross-margin expectations may not be achieved, that Chinese or other international suppliers may reduce prices, that logistics costs may change or that product pricing may not offset changes in operating costs, energy costs, labor costs, raw-material costs or financing costs. Competitive Risks: Risks arising from established global solar glass producers and new entrants, including pricing pressure, technological competition, scale advantages, overcapacity in parts of the value chain, import competition and the presence of larger, better-capitalized competitors. Technology & Product Risks: Risks that antimony-free solar glass, patterned solar glass, glass-glass module formats, bifacial module applications, fused silica, laser-based purification or other advanced materials strategies may face technical challenges, qualification delays, product-performance issues, adoption barriers or slower-than-expected market acceptance. Resource & Feedstock Risks: Risks that the quality, consistency, recoverability, processing behavior or suitability of silica from the Santa Maria Eterna project or other relevant feedstock sources may vary over time, may require additional testing, ongoing quality control or may not meet evolving technical, commercial or customer-specific requirements. Sand Metallurgy & Process Risks: Risks that further sand metallurgy, processing flow confirmation, beneficiation assumptions, quality-control requirements or product-specification work may identify additional technical requirements, costs, delays or constraints that could affect project economics, plant design or customer acceptance. Infrastructure & Logistics Risks: Risks related to transportation, roads, ports, export logistics, packaging, natural gas availability, grid access, energy infrastructure, utility connections, water availability, supply-chain constraints, contractor performance and broader infrastructure dependencies that could affect project timelines, costs or operating reliability. Energy & Utility Risks: Risks that electricity, natural gas, LPG backup, on-site photovoltaic generation or other utility assumptions may differ from expectations, that energy prices may increase, that infrastructure may not be available on expected terms or timelines or that utility contracts may not be finalized on terms consistent with the BFS. BDR Trading & Capital Markets Risks: Risks that the Sponsored BDR program and B3 listing may not achieve the anticipated benefits, that Brazilian investor participation may be lower than expected, that liquidity may remain limited, that arbitrage between B3 and the TSX Venture Exchange may not function as expected, that cross-market settlement or custody processes may create delays or constraints or that BDR-related share custody may affect trading dynamics, float, liquidity, valuation or price discovery. BDR Access & Investor Eligibility Caution: Statements regarding the Company’s BDR listing on B3, potential Brazilian investor participation, market access, liquidity, arbitrage, custody mechanics or institutional interest are subject to market, regulatory, operational and investor-eligibility factors. The existence of a BDR trading facility does not guarantee increased demand, liquidity, valuation support, institutional participation or favorable trading dynamics in Brazil, Canada or any other market. Share Price & Liquidity Risks: Risks related to share price volatility, trading liquidity, investor sentiment, promotional activity, market awareness, small-cap market conditions, Canadian and Brazilian trading dynamics and the possibility that capital markets may not recognize or value the Company’s milestones as expected. Phase 2 Expansion Risks: Risks that the potential second production line may not be advanced, financed, approved, permitted, built or operated, that Phase 1 may not provide the expected platform benefits, that shared infrastructure advantages may not materialize or that demand, financing, permitting, board approval or market conditions may not support future expansion. Macroeconomic & Geopolitical Risks: Risks related to inflation, interest rates, exchange-rate volatility, energy prices, commodity prices, geopolitical instability, trade policies, tariffs, import restrictions, supply-chain disruptions, political developments in Brazil or other jurisdictions and broader economic uncertainty that may impact financing, construction, operations or market conditions. Energy Market & Policy Risks: Risks that changes in energy policy, solar incentives, net-metering rules, distributed-generation frameworks, industrial policy, local-content rules, renewable-energy targets, fossil fuel pricing dynamics or broader energy-transition policies may influence the pace of solar adoption and the overall market opportunity. Environmental & ESG Risks: Risks that environmental, social or governance considerations may impose additional costs, constraints or delays or that anticipated ESG advantages, including antimony-free product positioning, local production, reduced logistics exposure or lower-carbon manufacturing assumptions, may not translate into expected commercial or financial benefits. Foreign Exchange & Taxation Risks: Risks related to foreign-exchange volatility, differences between USD, CAD, BRL and EUR exposures, local taxation, VAT, duties, incentives, transfer pricing, cash-flow treatment, inflation, depreciation assumptions and the possibility that tax or currency outcomes may differ from those assumed in project planning. Operational Ramp-Up Risks: Risks that the plant may not ramp up according to the schedule, yield assumptions, production volumes, quality targets, cost profile or efficiency improvements assumed in the BFS and that startup, commissioning, workforce training, equipment performance or customer qualification may take longer or cost more than expected. Force Majeure & External Events: Risks arising from natural disasters, extreme weather, pandemics, labor disruptions, civil unrest, political instability, accidents, equipment failures, supply interruptions, contractor disruptions or other events beyond the Company’s control. Comparative Information, Valuation Metrics & Non-Equivalence Caution: References in this report to other companies, mining projects, feasibility studies, preliminary economic assessments, development-stage assets, NPV, IRR, CAPEX, payback periods, margins, production profiles, market capitalizations or other financial or technical metrics are provided for illustrative context only and should not be relied upon independently. Such comparisons may not be directly comparable to Homerun, its proposed solar glass manufacturing facility or its broader business strategy. Mining projects and industrial manufacturing projects may differ materially in geology, permitting, financing structure, commodity exposure, operating risk, construction risk, market dynamics, cost structure, customer concentration, taxation, jurisdictional framework, technical requirements and revenue model. No comparison should be interpreted as implying that Homerun will achieve similar results, valuations, financing outcomes, construction timelines, operating performance or market recognition. In addition, valuation multiples, EV/EBITDA comparisons, specialty-materials benchmarks, industrial-platform frameworks, replacement-cost discussions, margin comparisons and public-company examples referenced throughout the report or accompanying slides are illustrative only, may rely on third-party market data, may change materially over time and should not be interpreted as indicating that Homerun will achieve similar trading multiples, earnings quality, valuation premiums, scalability characteristics or market positioning. Accordingly, readers should not place undue reliance on forward-looking information. Rockstone and the author of this report do not undertake any obligation to update any statements made in this report except as required by law. Past performance, comparisons to other companies, projects, commodities, technologies, jurisdictions, feasibility studies, capital-market events or industry trends are provided for illustrative purposes only and should not be considered indicative of future results.

Disclosure of Interest and Advisory Cautions: Nothing in this report should be construed as a solicitation to buy or sell any securities mentioned. Rockstone, its owners and the author of this report are not registered broker-dealers or financial advisors. Before investing in any securities, you should consult with your financial advisor and a registered broker-dealer. Never make an investment based solely on what you read in an online or printed report, including Rockstone’s report, especially if the investment involves a small, thinly-traded company that isn’t well known. The author of this report, Stephan Bogner, is paid by Homerun Resources Inc. On September 8, 2025, Homerun announced that the company “entered into an agreement with Rockstone Research to provide marketing services to the company”, and that “Rockstone Research is an arm’s-length marketing firm and has been engaged for an initial three-month term for total consideration of $25,000, which is payable up front. The company does not propose to issue any securities to Rockstone in consideration for the services to be provided to the company.” The author owns equity of Homerun and thus will profit from volume and price appreciation of the stock. This also represents a significant conflict of interest that may affect the objectivity of this reporting. The author may buy or sell securities of Homerun (or comparable companies) at any time without notice, which may give rise to additional conflicts of interest. Overall, multiple conflicts of interests exist. Therefore, the information provided in this report should not be construed as a financial analysis or recommendation but as an advertisement. This report should be understood as a promotional publication and does not replace individual investment advice. Rockstone’s and the author’s views and opinions regarding the companies that are featured in the reports are the author‘s own views and are based on information that was received or found in the public domain, which is assumed to be reliable. Rockstone and the author have not undertaken independent due diligence of the information received or found in the public domain. Rockstone and the author of this report do not guarantee the accuracy, completeness, or usefulness of any content of this report, nor its fitness for any particular purpose. Lastly, Rockstone and the author do not guarantee that any of the companies mentioned in the reports will perform as expected, and any comparisons that were made to other companies may not be valid or come into effect. For the avoidance of doubt, this report is not intended for distribution to, or use by, any person or entity in any jurisdiction where such distribution, publication or use would be contrary to local law or regulation. Readers are solely responsible for ensuring that their review and use of this report is lawful in their jurisdiction. Neither Rockstone nor the author accepts liability for any direct or indirect loss arising from the use of this report or from any investment decision made in reliance on it. Please read the entire Disclaimer carefully. If you do not agree to all of the Disclaimer, do not access this website or any of its pages including this report in form of a PDF. By using this website and/or report, and whether or not you actually read the Disclaimer, you are deemed to have accepted it. Information provided is educational and general in nature and should not be interpreted as personalized investment, financial, legal, tax or professional advice. Data, tables, figures and pictures, if not labeled or hyperlinked otherwise, have been obtained from Stockwatch.com, Tradingview.com, Homerun Resources Inc. and the public domain. The cover picture has been obtained and licenced from 123rf.com.