There are stages in a company’s evolution when the investment narrative begins to change in substance, not just in tone. A resource company that was once assessed mainly on exploration potential can begin to be valued for something far broader: Strategic relevance, industrial scalability and the ability to execute on a real-world supply chain opportunity.

For Homerun Resources Inc., that transition is now taking shape. With the release of a positive Bankable Feasibility Study (BFS) for its planned solar glass manufacturing plant in Belmonte, Bahia, Brazil, Homerun has moved beyond the conceptual stage of vertical integration, high-purity silica and energy-transition manufacturing.

The company has now delivered a bankable technical and financial blueprint for a large-scale industrial asset designed to serve Brazil’s rapidly expanding solar market and selected export markets across the Americas.

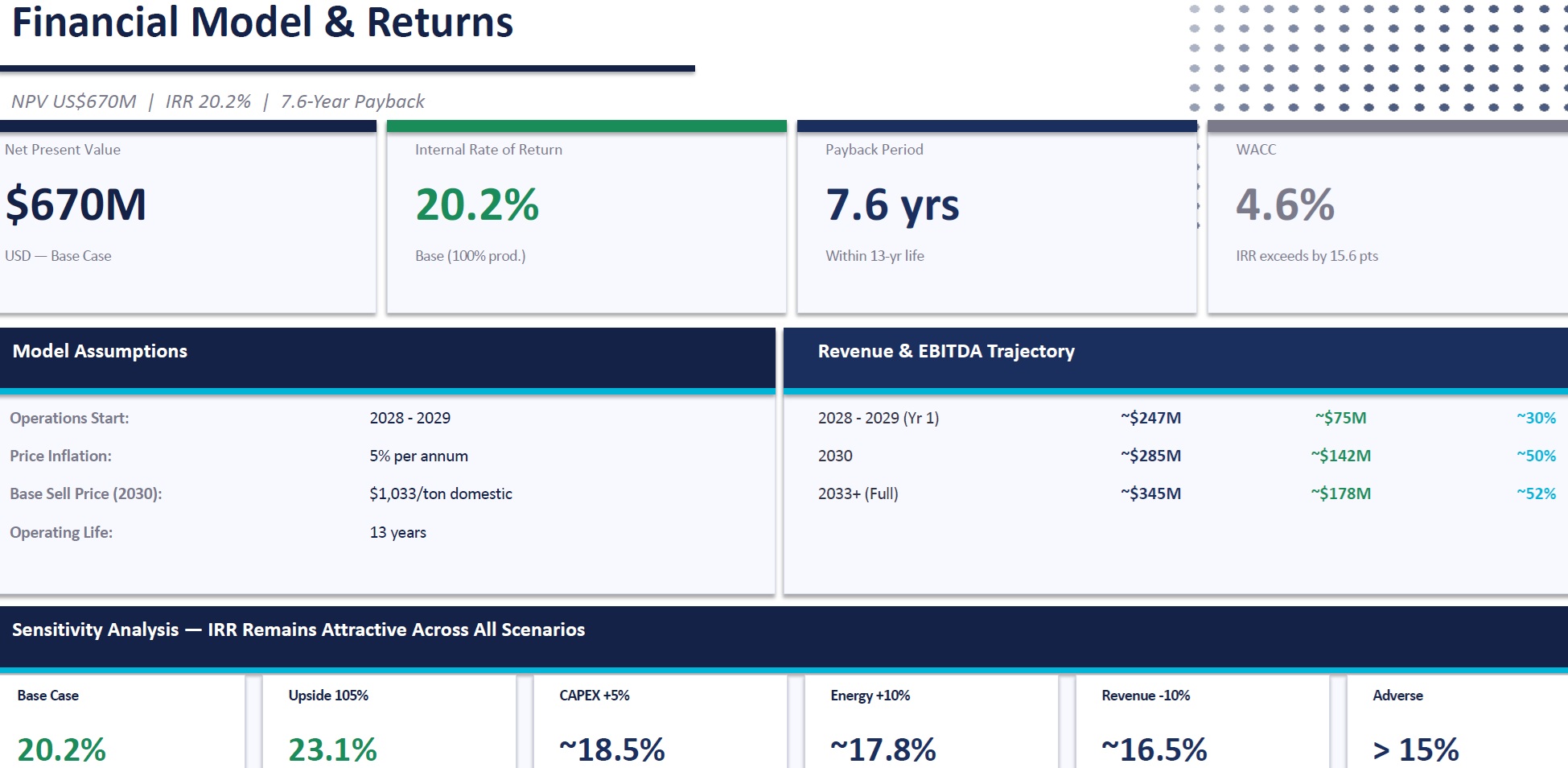

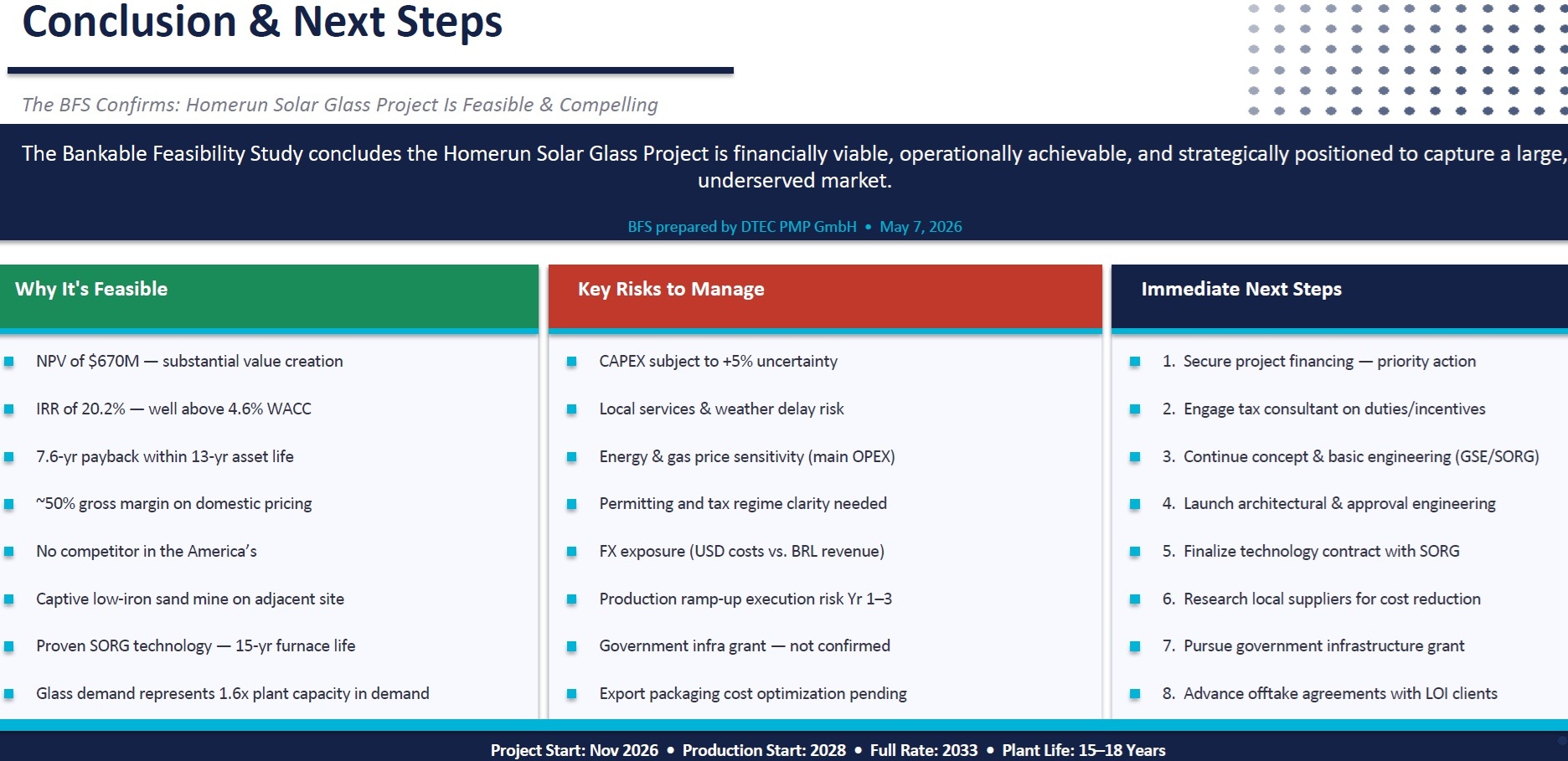

The BFS outlines a base-case NPV of ~670 million USD, an IRR of 20.2%, total initial CAPEX of ~$396.5 million USD and an estimated payback period of 7.6 years. At 105% production, the NPV rises to ~$829 million USD and the IRR to 23.1%.

The importance of these numbers is not that they look impressive on a slide. The importance is that they explain why Homerun is now entering a very different conversation with financiers, strategic partners, offtake customers and institutional investors.

A resource story has become a bankable infrastructure platform. At the same time, Homerun opened a Brazilian capital-markets door in the country where this project is being built: Its Sponsored Brazilian Depositary Receipts (BDRs) now trade on B3 under HMRN31, with each BDR representing 1 common Homerun share.

In simple terms: The BFS makes the project financeable. The B3 listing makes the investment accessible in Brazil, giving domestic investors a direct way to participate in a company advancing an industrial project aligned with Brazil’s solar growth and strategic manufacturing ambitions. Together, they mark a decisive shift in Homerun’s capital-markets profile.

From Vision To Verification

A true BFS acts as a reality check rather than promotional material. For Homerun, the study now provides the technical and economic blueprint that lenders, strategic investors and infrastructure financiers can use to assess whether the Belmonte plant can be financed, built and operated within a defined risk framework.

For private investors, that matters. Exploration companies often publish attractive geological potential, while development companies may release preliminary economic models. A BFS represents a higher standard. It forces the company to define engineering, capacity, capital cost, operating cost, product pricing, margins, timelines, risks and next steps in a format serious capital providers can evaluate.

Homerun’s BFS confirms the technical and economic feasibility of a 1,000 tonne per day (tpd) soda-lime patterned solar glass facility in Belmonte, Bahia. The plant is designed with 4 roll glass lines of 250 tpd each, up to 1,100 tpd of furnace capacity, 4 processing lines, an on-site PV system and glass thicknesses from 1.8 mm to 4 mm.

It is expected to produce ultra-clear patterned glass for mono and bifacial photovoltaic modules, with production projected to ramp from ~239,000 tonnes per year (tpy) in the first operating year to ~288,300 tpy from Year 5 onward.

That scale matters. Homerun is moving beyond laboratory work and niche demonstration toward a full industrial manufacturing platform designed to serve a real solar supply-chain gap in Brazil and potentially selected export markets, with scale, margin and strategic relevance now defined in bankable detail for the first time.

In other words, Homerun’s strategy is about converting a low-cost raw material advantage into a high-value industrial product. That is the difference between operating as a quarry and becoming a strategic manufacturer.

The Numbers

The headline number is the NPV: 670 million USD in the base case. NPV means Net Present Value. It is the estimated value today of future project cash flows after applying a discount rate. NPV differs from market capitalization and should not be treated as guaranteed money in the bank. Instead, it is one of the central tools used to judge whether a project creates value.

In Homerun’s case, the NPV is ~1.7 times the initial CAPEX of 396.5 million USD. That is important because it suggests that the projected value of the asset is meaningfully larger than the upfront capital required to build it. For a capital-intensive manufacturing project, that is a strong starting point.

The IRR is 20.2% in the base case. IRR means Internal Rate of Return. It shows the expected annualized return of the project. The BFS compares this IRR with an estimated WACC of 4.6%. WACC means Weighted Average Cost of Capital, or roughly the blended cost of debt and equity funding. When a project’s IRR is far above its cost of capital, it indicates value creation. In Homerun’s case, the spread is ~15.6 percentage points.

That is the key sentence for investors: The project is not merely profitable in the model. It is projected to earn returns far above its estimated cost of funding.

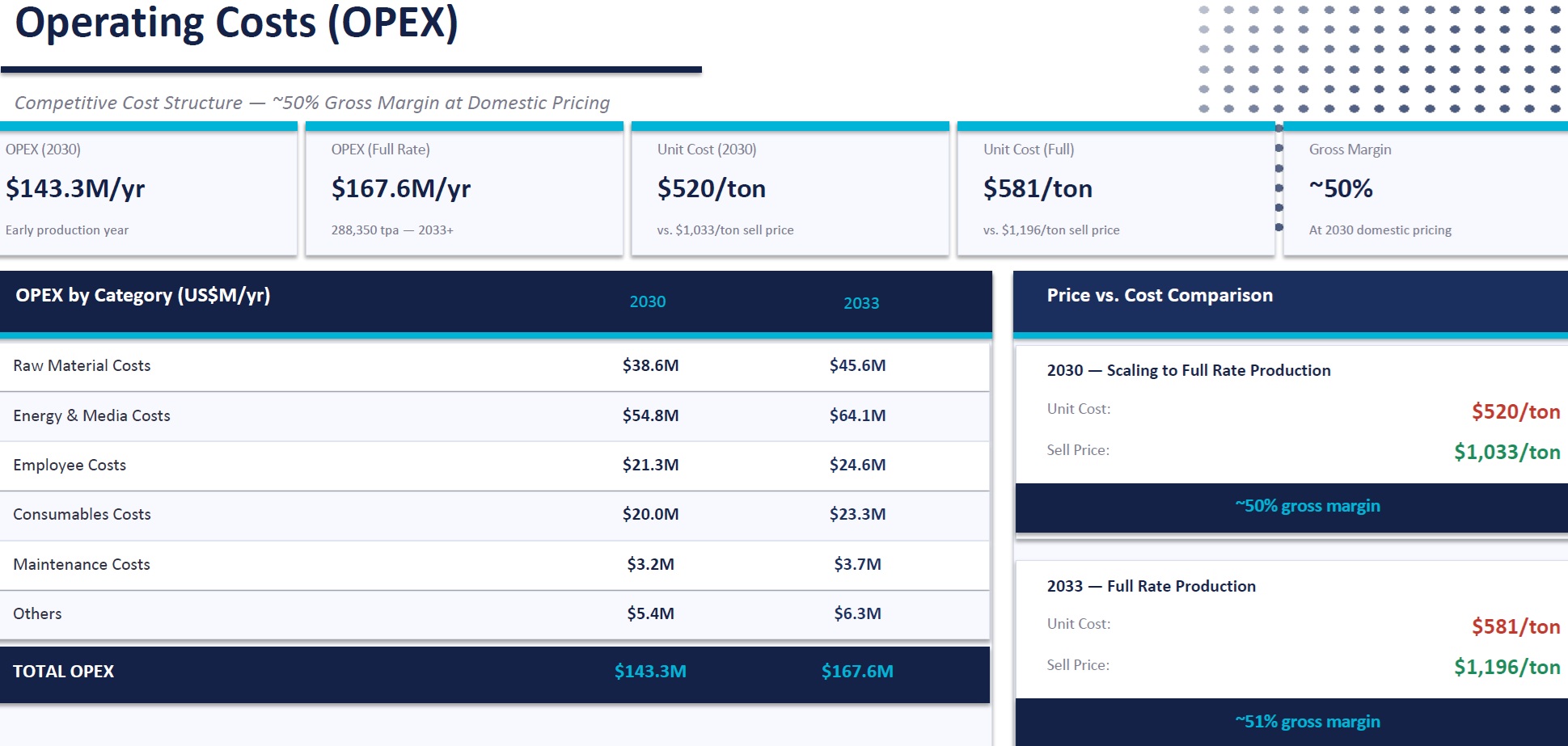

The gross margin is another important metric. The BFS estimates operating costs of ~520 USD/t by 2030 compared with projected domestic selling prices of ~1,033 USD/t. By 2033, estimated operating costs are ~581 USD/t compared with projected selling prices of ~1,196 USD/t. That translates into an indicative gross margin of roughly 50% to 51%.

Here, the economics become much easier to understand: If Homerun can manufacture solar glass at roughly half the domestic selling price, the plant has room to absorb cost volatility, ramp-up inefficiencies and financing costs while still generating substantial cash flow. At full production, the model points to annual revenue of ~344.9 million USD and OPEX of ~167.6 million USD. That implies an operating spread of roughly 177 million USD per year before items such as depreciation, financing, taxes and corporate costs.

The CAPEX therefore needs context. 396.5 million USD is a large number. For a junior company, it is very large. But for an industrial facility capable of generating hundreds of millions of dollars in annual revenue and a 50% gross margin, the number is not outlandish. At full-rate production, the CAPEX is roughly 1.15 times projected annual revenue and about 2.2 times the implied annual operating spread, placing the investment requirement in a very different context than the headline figure alone suggests.

That is the value of the BFS: It gives investors a way to judge whether the plant is expensive or cheap relative to what it is designed to earn. And on that basis, the CAPEX looks less like a burden and more like the price of entry into a high-margin industrial platform. The real question is no longer whether the number is large, but whether the return profile justifies it – and the BFS suggests that it does.

Mining Benchmarks: How Homerun Stacks Up

Many Homerun shareholders, including the author of this report, think in resource-sector terms. They understand gold, copper, lithium and uranium projects. Solar glass manufacturing is less familiar, which makes a comparison with conventional mining projects especially useful.

A good mining project is usually judged by the same basic questions: How much does it cost to build? How much value does it create? How fast is the payback? How sensitive is it to prices and costs? How much risk remains before financing and construction?

By those standards, Homerun’s BFS looks highly competitive, especially for a company attempting to build a strategic first-mover manufacturing asset rather than a conventional mine. For example:

- B2Gold’s Gramalote Gold Project in Colombia: PEA (Preliminary Economic Assessment) reported an after-tax NPV of 778 million USD, an after-tax IRR of 20.6%, a payback of 3.1 years and pre-production capital of 807 million USD. The IRR is almost identical to Homerun’s base-case IRR, while the capital requirement is roughly twice as large.

- Osino’s Twin Hills Gold in Namibia: DFS (Definitive Feasibility Study) reported a post-tax NPV of 480 million USD, a post-tax IRR of 28%, a 2.2-year payback and overall capital cost of 365 million USD. That is a very strong gold project and its payback is faster than Homerun’s, but its NPV is lower than Homerun’s base-case NPV despite a similar construction-capital range.

- Skeena’s Eskay Creek Gold-Silver in British Columbia: DFS reported an after-tax NPV of 2 billion CAD, an IRR of 43%, a 1.2-year payback and pre-production CAPEX of 713 million CAD, with a reported NPV:CAPEX ratio of 2.8:1. That is an exceptional mining benchmark, not an average one. Homerun’s NPV:CAPEX ratio of about 1.7:1 is below that elite gold-project example, but it is still robust for an industrial manufacturing plant with a strategic import-substitution thesis.

Homerun has moved beyond the speculative language of exploration upside. With the BFS, investors now have feasibility-level economics for a manufacturing project that can be measured against serious resource-development benchmarks.

Homerun’s end product is solar glass rather than gold doré or copper concentrate: A critical input for photovoltaic modules, a strategic industrial product and something Brazil currently imports rather than manufactures domestically, despite its enormous solar potential.

There is another important distinction: Solar glass is only one vertical within Homerun’s broader platform. While many traditional resource juniors are built around a single deposit and a single commodity pathway, Homerun is developing multiple connected verticals across silica, solar, energy storage and energy solutions. If executed successfully, that could provide broader growth leverage than a conventional single-project model.

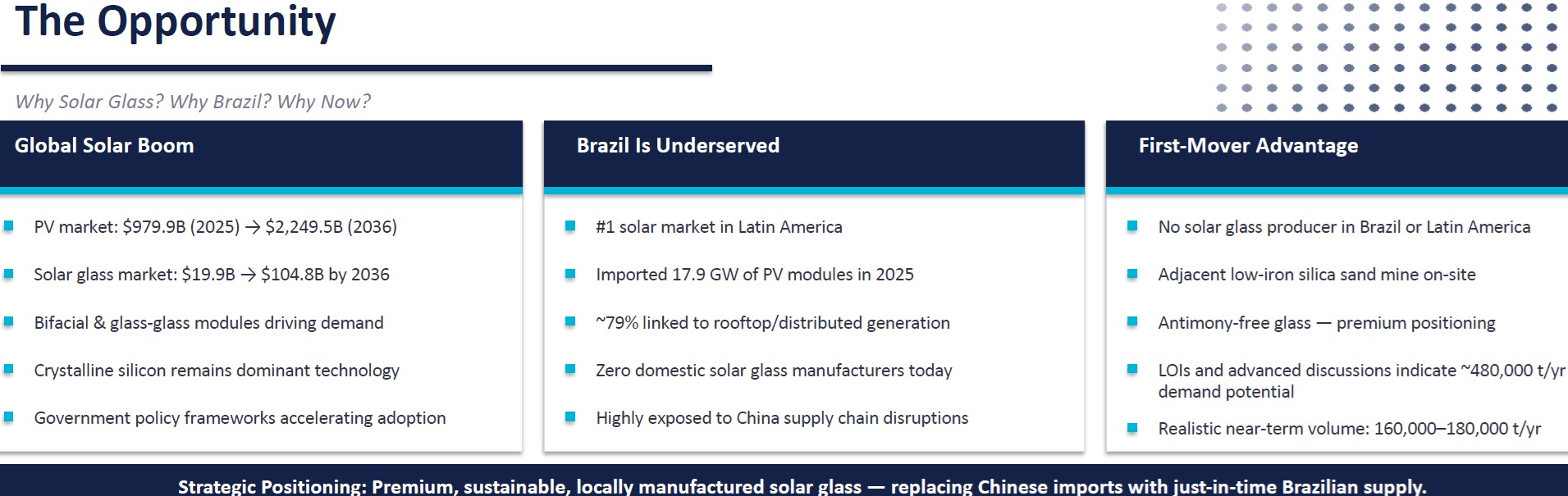

Brazil’s Solar Glass Gap

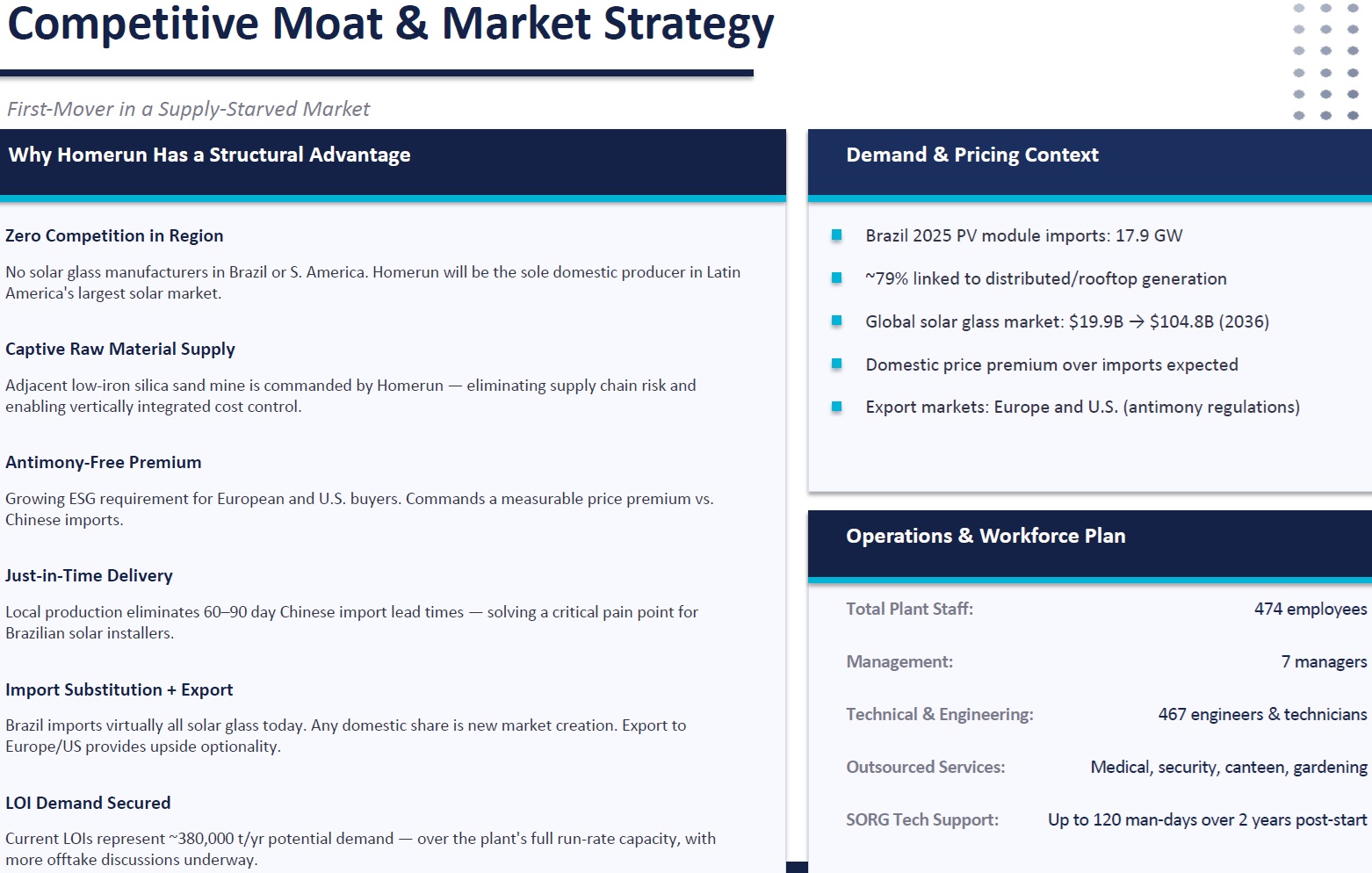

The BFS goes beyond plant economics. It highlights a strategic supply-chain gap in Brazil’s solar market. Brazil is identified in the BFS as the leading solar market in Latin America, yet the country remains highly dependent on imported PV modules and solar glass.

The BFS notes that Brazil imported ~17.9 GW of PV modules in 2025, with roughly 79% tied to distributed generation, underscoring the strength of rooftop and decentralized solar demand.

Homerun’s BFS presentation also highlights a critical gap: Brazil has no domestic solar glass manufacturer today, positioning Homerun as a first mover in traditional patterned solar glass production in the Americas.

At the center of the investment case is a simple point: Solar glass is a critical performance layer inside every photovoltaic module, not a cosmetic add-on. It must be exceptionally clear, durable, consistent and optimized for light transmission. Homerun’s BFS presentation specifies light transmission above 94%, including anti-reflective coating, with product formats designed for both mono and bifacial PV modules.

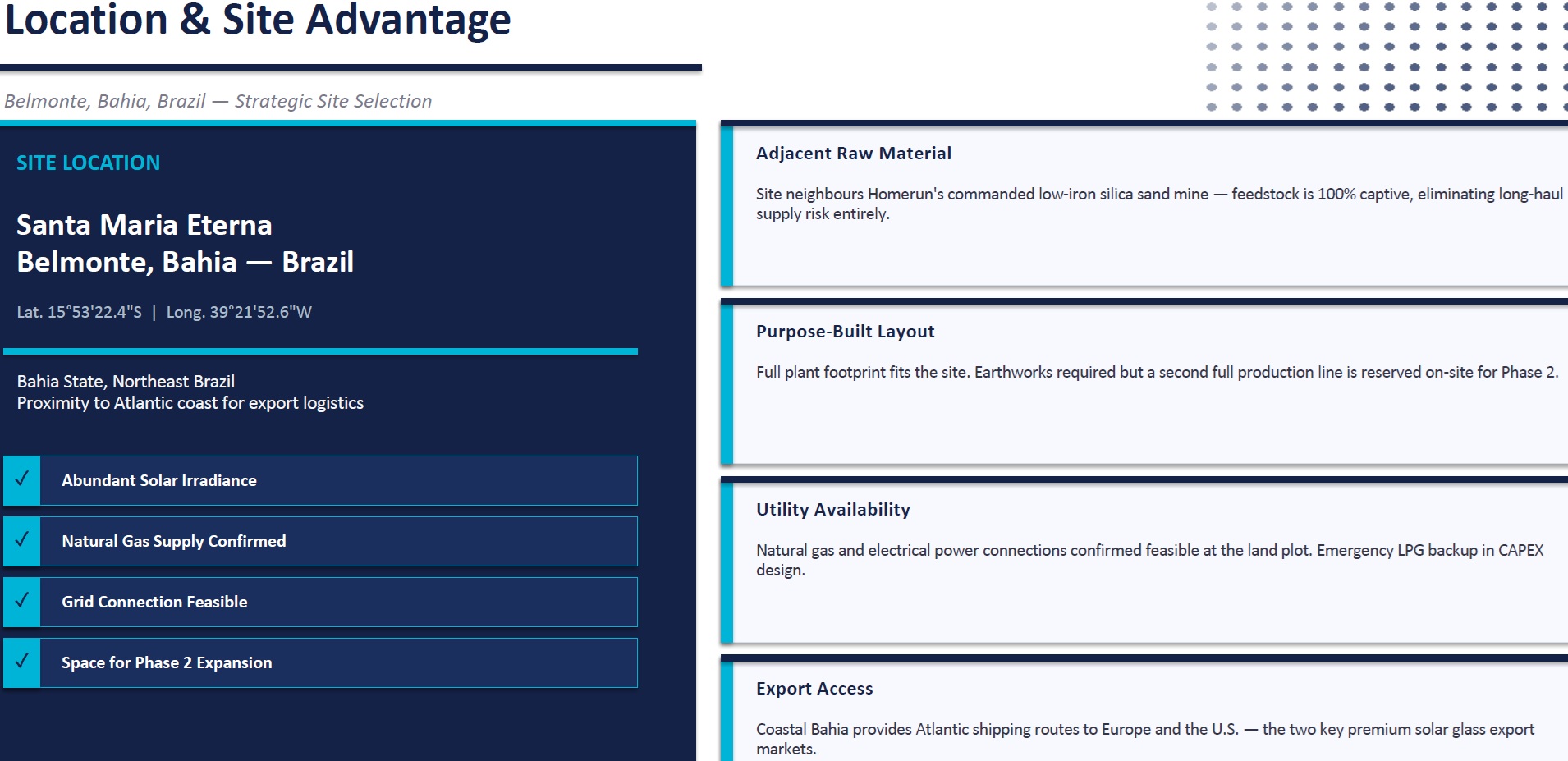

Brazil has solar demand. Brazil has sunlight. Brazil has industrial ambition. Homerun adds the missing industrial link: A planned solar glass manufacturing site in Bahia, secured low-iron silica sand at Belmonte and a BFS for domestic production. That combination is rare.

The BFS presentation describes the site as strategically positioned with captive raw material supply, feasible natural gas and grid connections, Atlantic coastal export access and room for a potential second production line.

The location matters because it is part of the economic advantage, not just a point on the map. A solar glass plant without secure silica supply is exposed to raw-material risk. A silica deposit without value-added processing remains a lower-margin materials story. Homerun aims to connect both sides: Captive feedstock and high-value manufacturing.

That is vertical integration at its most strategic.

Built to Win: Homerun’s Structural Edge

The BFS outlines several elements that could give Homerun a rare structural edge in the solar glass market.

- The plant is planned next to Homerun’s low-iron silica sand resource. That reduces long-haul feedstock risk and gives the company a captive raw-material advantage.

- The facility is designed around proven glass manufacturing technology. The presentation identifies SORG GmbH as the technology partner and notes a 15-year furnace campaign life, up to 10% furnace overcapacity, processing-line overcapacity and post-startup technical support.

- The product is positioned as antimony-free solar glass. The presentation describes this as premium positioning and connects it with ESG-related demand from European and US buyers.

- The project is entering a market where Homerun believes there is no current solar pattern glass manufacturer in the Americas. Today’s news-release explicitly highlights the absence of an identified current solar pattern glass manufacturer in the Americas and the presentation repeatedly frames the project around first-mover advantage.

- Demand indications appear larger than Phase 1 capacity. The BFS cites existing letters of intent (LOIs) indicating potential demand of ~380,000 tpy, with additional advanced discussions indicating demand of 480,000 tpy. After adjustment, the BFS refers to realistic secured local volume of ~160,000-180,000 tpy.

This deserves careful interpretation. LOIs are not binding offtake contracts and do not guarantee revenue, but they show that the market is not theoretical. At full production of ~288,300 tpy, even the adjusted 160,000-180,000 tpy local volume would represent more than half of Phase 1 capacity. The larger 480,000 tpy demand indication is roughly 1.6 times Phase 1 full-rate production.

However, the likely financing sequence may not require every LOI to become definitive first. Given the strategic nature of domestic solar glass production, Brazil’s import dependence and the project’s industrial-policy relevance, the first major funding step could come through state-driven, development-bank or public-sector-supported financing. Binding offtake agreements would still be important, but they may develop alongside the financing process rather than before it.

For investors, that is a crucial distinction: The BFS does not simply start a customer-contracting process. It gives government-linked financiers, strategic partners and infrastructure investors the technical and economic basis to begin underwriting a project that could strengthen Brazil’s solar supply chain. In other words, the BFS may open the financing door before the final commercial contracts are fully locked in.

The next phase is therefore about maturing several conversations at once: Financing, offtake, permitting, utilities, engineering and executable construction contracts.

The B3 Listing

The recent B3 listing announcement on May 5 deserves to be read together with the BFS. Homerun’s Sponsored BDRs now trade on B3 under the ticker HMRN31. The ratio is 1:1, meaning 1 BDR represents 1 common Homerun share. The company explains that qualified Brazilian investors buying BDRs on B3 can cause the depositary to source underlying shares from the TSX-V market or existing blocked inventory, linking the Brazilian trading instrument to the Canadian-listed float.

This matters for 2 reasons:

- It gives Brazilian investors a local-market vehicle to participate in a project located in Brazil. That includes domestic institutions, family offices and high-net-worth investors the company explicitly says it aims to reach.

- The timing is powerful. A B3 listing before or around a BFS is not just another ticker symbol. It creates a capital-markets bridge at the moment the project becomes financeable.

Many institutional investors cannot easily invest in early-stage stories that lack feasibility-level economics. Some mandates require more technical certainty. Others need local-market access, custody compatibility, liquidity visibility or a clearer project-finance pathway. The BFS does not automatically unlock every institution, but it makes Homerun a more credible candidate for serious due diligence.

That is the key shift: Homerun now has a Brazilian project, a Brazilian trading instrument and a bankable feasibility document for a Brazilian manufacturing plant designed to serve Brazil’s solar market. The geography of the asset and the geography of potential capital are beginning to align.

And that capital-markets alignment becomes even more important when investors look beyond Phase 1.

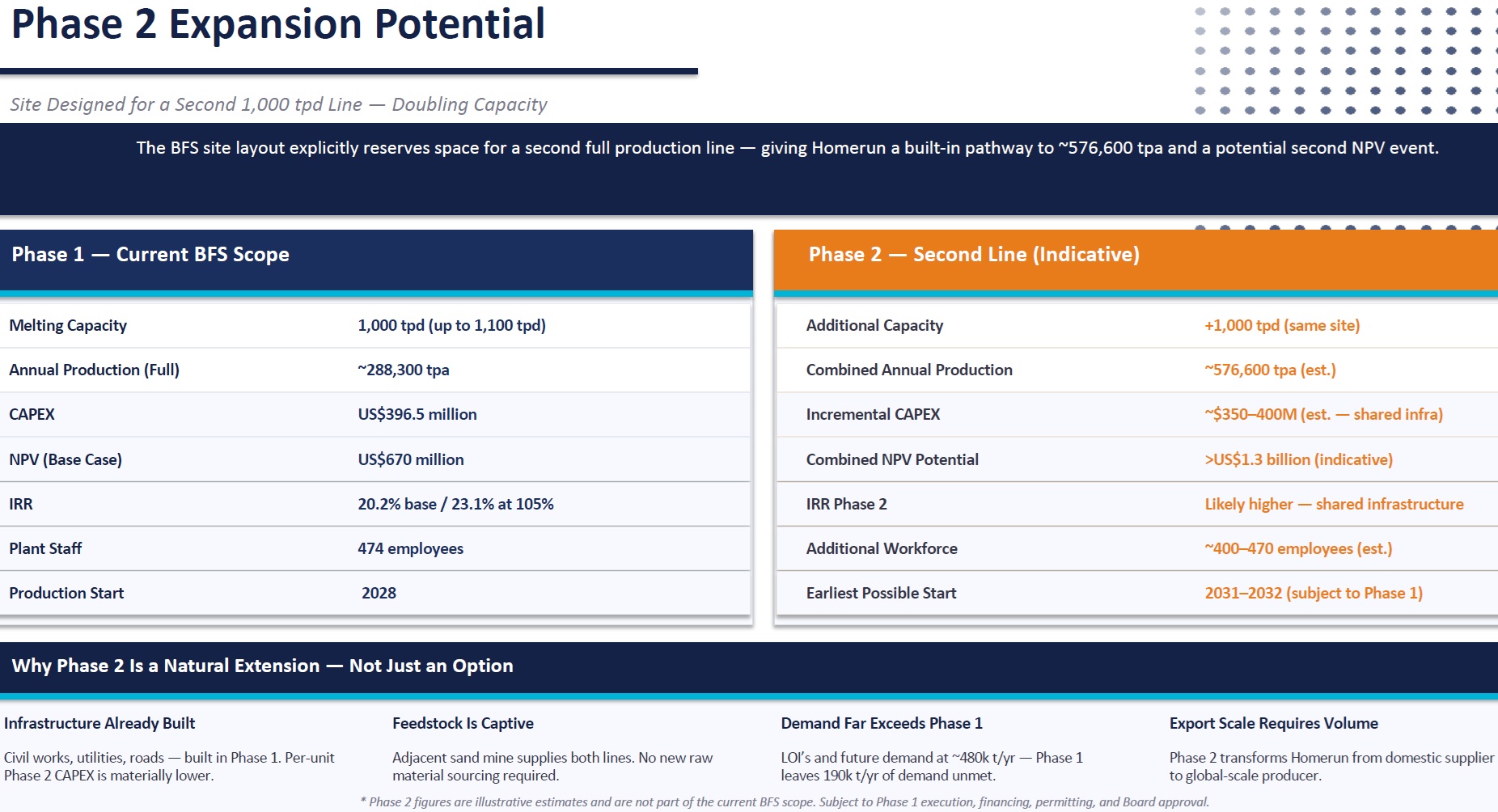

The Built-In Path to Scale: Phase 2

One of the most interesting elements in the BFS presentation is the Phase 2 potential. Page 10 states that the site layout explicitly reserves space for a second full 1,000 tpd production line. The presentation frames this as a pathway to ~576,600 tpy of combined annual production and a potential second NPV event.

This is important because investors often underestimate the value of industrial platforms. A first plant carries a heavy upfront burden: Land, civil works, utilities, infrastructure, local permitting, workforce creation, engineering learning and supplier networks.

If a second line can share part of that infrastructure, the second phase can sometimes be economically stronger than the first, with lower execution friction, faster scaling potential and better capital efficiency than a standalone greenfield project.

To be clear, Phase 2 is not part of the current BFS scope. It will require financing, permitting, board approval and possibly successful Phase 1 execution. But strategically, it changes the lens through which investors should view Homerun, because the first plant could become proof of concept for a much larger regional manufacturing footprint.

Phase 1 could become more than a plant: The foundation of a regional solar glass manufacturing platform.

From BFS to Execution

The BFS is not the finish line, but the starting line for execution. The next steps likely include independent review of the financial model, independent taxation and cash-flow evaluation, sand metallurgy confirmation, permitting, pre-engineering, utility contract negotiations, project financing and binding supply agreements. These are listed in today’s news-release as immediate next steps, with several targeted for Q2 or Q3 2026.

Investors should watch those milestones closel:

- A signed financing package would be a major de-risking event.

- Binding offtake agreements would validate market demand.

- Utility contracts would strengthen operating-cost assumptions.

- Permitting progress would reduce timeline risk.

- Detailed engineering would narrow the construction-risk band.

Each step would move Homerun further away from concept risk and closer to shovel-ready industrial execution.

This is how a feasibility-stage project becomes a financed construction project, and ultimately, how a strategic supply-chain vision can become a real manufacturing asset.

Bottom Line

Homerun’s BFS is important because it gives investors structured answers to the questions they should be asking, while reframing the company’s path from resource potential to industrial execution:

- Is the project technically feasible? The BFS says yes.

- Is the project economically attractive? A 670 million USD base-case NPV, 20.2% IRR and ~50% gross margin suggest yes.

- Is the CAPEX large? Yes, but it appears proportionate to the plant’s projected revenue, margin and strategic market position.

- Is the payback instant? No. At 7.6 years, the project should be viewed less like a quick-flip mine and more like an industrial platform. Large solar infrastructure projects are often evaluated over multi-year payback horizons, with some industry sources citing 5-10 years as a typical range for solar power plants. Homerun’s 7.6-year payback therefore appears reasonable for a long-life industrial asset, especially one designed to build durable manufacturing capacity rather than chase a short-term commodity cycle.

- Is the market real? Brazil’s solar demand, import dependence and the absence of a current regional solar glass producer suggest a compelling and potentially strategic market opening, particularly as Brazil continues expanding domestic solar deployment while still relying heavily on imported photovoltaic components and materials. That creates a rare opportunity for local manufacturing to reduce supply-chain risk, shorten delivery times, capture value inside Brazil and support long-term industrial resilience.

- Is the company now in position to attract more serious capital? The BFS and B3 listing together make that far more plausible than before.

That is why this milestone matters: Homerun has not merely published a set of numbers. It has placed a bankable industrial plan in front of financiers, institutions, strategic partners and the Brazilian market.

In the resource sector, value is often created when rock becomes a mine. In Homerun’s case, value may be created when silica becomes solar glass, when solar glass becomes domestic supply and when domestic supply becomes strategic infrastructure for Brazil’s energy transition.

The BFS is where the strategy becomes measurable, financeable and real, turning a bold industrial vision into a defined execution pathway.

Company Details

Homerun Resources Inc.

#2110 – 650 West Georgia Street

Vancouver, BC, V6B 4N7 Canada

Phone: +1 844 727 5631

Email: info@homerunresources.com

www.homerunresources.com

ISIN: CA43758P1080 / CUSIP: 43758P

Shares Issued & Outstanding: 77,086,618

Canada Symbol (TSX.V): HMR

Current Price: 1 CAD (05/11/2026)

Market Capitalization: 77 Million CAD

Germany Ticker / WKN: 5ZE / A3CYRW

Current Price: 0.615 EUR (05/11/2026)

Market Capitalization: 47 Million EUR

Stephan Bogner

Contact

Rockstone News & Research

Stephan Bogner (Dipl. Kfm., FH)

Müligässli 1, 8598 Bottighofen

Switzerland

Phone: +41-71-5896911

Email: info@rockstone-news.com

Disclaimer and Information on Forward Looking Statements: Rockstone and Homerun Resources Inc. (“Homerun“) caution investors that any forward-looking information provided herein is not a guarantee of future results or performance, and that actual results may differ materially from those in forward-looking information as a result of various factors. The reader is referred to Homerun’s public filings for a more complete discussion of such risk factors and their potential effects, which may be accessed through its documents filed on SEDAR+ at www.sedarplus.ca. All statements in this report, other than statements of historical fact, should be considered forward-looking statements. Much of this report is comprised of statements of projection. Such statements involve known and unknown risks, uncertainties and other factors that may cause actual results or events to differ materially from those anticipated in these forward-looking statements. There can be no assurance that such statements will prove to be accurate, as actual results and future events could differ materially from those anticipated in such statements. Forward-looking statements in this report include expectations related to the commercial, strategic, financial and market implications of Homerun’s completed Bankable Feasibility Study (“BFS”) for its proposed antimony-free solar glass manufacturing facility in Bahia, Brazil, including assumptions that the BFS may support project financing discussions, strategic partnership opportunities, offtake negotiations, permitting activities, construction planning and the Company’s transition into the next phase of development. Forward-looking statements also include expectations regarding the interpretation and potential impact of the BFS results, including assumptions that the reported project economics, including NPV, IRR, CAPEX, OPEX, gross margin, payback period, production capacity, ramp-up profile, sensitivity cases and other financial or technical metrics, may provide a useful basis for evaluating the project’s potential viability, bankability, strategic relevance and possible attractiveness to financing partners, strategic investors and future commercial counterparties. Forward-looking statements further include expectations regarding project financing, including assumptions that discussions with prospective financing partners, state-linked financing sources, development banks, infrastructure investors, strategic partners or other funding sources may progress, that indicative interest may translate into structured financing arrangements and that the Company may secure sufficient capital on acceptable terms to support detailed engineering, project development, construction and initial operations. Additional forward-looking statements include expectations related to the Company’s Sponsored Brazilian Depositary Receipt (“BDR”) program and listing on the B3 stock exchange, including assumptions that the listing may broaden and diversify the shareholder base, may facilitate increased participation from Brazilian institutional investors, family offices, high-net-worth individuals and other qualified investors and may improve the Company’s visibility in the country where its core operations and growth projects are located. Forward-looking statements also include expectations regarding the potential market impact of the BDR structure, including assumptions that demand for BDRs may lead to the acquisition and custody of underlying shares from the TSX Venture Exchange in Canada, may influence trading dynamics and may affect liquidity, float, valuation, arbitrage activity and price discovery over time. Forward-looking statements further include expectations regarding market positioning and industry relevance, including assumptions that Homerun’s high-purity low-iron silica, antimony-free solar glass strategy and vertically integrated platform may align with increasing demand for solar materials, advanced glass, domestic manufacturing, energy infrastructure and supply-chain resilience and may support long-term commercial opportunities across multiple segments of the energy transition. Additional forward-looking statements relate to the Company’s broader platform strategy, including assumptions that Homerun may advance its 4 core verticals, Silica, Solar, Energy Storage and Energy Solutions, and that its silica resource in Bahia may support downstream processing, solar glass manufacturing, advanced materials, long-duration energy storage applications, laser-based purification technologies and related energy applications over time. Forward-looking statements are also made with respect to execution, development and scaling, including assumptions that the Company may successfully advance from feasibility to financing, from financing to construction and from construction to commercial operations, and that timelines, costs, operating parameters, product specifications, customer demand, infrastructure access and ramp-up assumptions may remain within expected ranges. Forward-looking statements also include expectations related to Phase 2 expansion potential, including assumptions that the site may support a second 1,000 tonne per day production line, that shared infrastructure may improve future capital efficiency, that demand may support additional capacity and that any future expansion may create additional value beyond the current BFS scope. Forward-looking statements are based on current expectations, estimates and assumptions that are inherently subject to uncertainty and may differ materially from actual outcomes. Forward-looking statements are subject to risks and uncertainties including, but not limited to: BFS Interpretation & Model Assumption Risks: Risks that the BFS, while completed, may rely on assumptions, estimates, forecasts, vendor quotations, technical inputs, market data, inflation assumptions, operating-cost assumptions, pricing assumptions, taxation assumptions, discount-rate assumptions or sensitivity cases that may prove inaccurate, incomplete or subject to material revision over time. Financing Risks: Risks that project financing may not be secured on acceptable terms or within expected timeframes, that state-driven, development-bank, infrastructure, strategic or private financing sources may not provide binding commitments, that indicative interest may not convert into executable funding arrangements or that financing conditions may change due to market, macroeconomic, political or project-specific factors. Public-Sector & Development Financing Caution: Statements regarding potential state-linked, development-bank, infrastructure, public-sector-supported or strategic financing are forward-looking and subject to significant uncertainty. There can be no assurance that any government-related or development-finance institution will provide funding, guarantees, incentives, infrastructure support, concessional terms or any other form of financial assistance, or that any such support would be available on terms acceptable to the Company. Construction & Development Risks: Risks associated with advancing from feasibility to construction, including engineering challenges, cost overruns, contractor performance, equipment availability, permitting delays, weather-related delays, infrastructure limitations, local-service constraints, procurement delays and execution risks typical of large-scale industrial manufacturing projects. Permitting & Regulatory Risks: Risks related to environmental approvals, land use, industrial permitting, mining regulations, installation approvals, operating licenses, export controls, taxation, customs duties, local incentives, regulatory interpretation or other legal requirements in Brazil or other relevant jurisdictions. Offtake & Customer Commitment Risks: Risks that existing letters of intent, demand indications, advanced discussions or non-binding commercial expressions may not convert into definitive binding supply agreements, may be delayed, may be renegotiated on less favorable terms or may not generate the expected level of revenue, pricing visibility or bankability support. Market Demand & Industry Risks: Risks that demand for solar glass, photovoltaic modules, high-purity silica or related materials may develop more slowly than expected, may be impacted by changes in solar deployment trends, interest rates, policy frameworks, subsidies, competing technologies, import dynamics or regional imbalances and may be subject to cyclical or structural market changes. Pricing & Margin Risks: Risks that projected domestic selling prices, export pricing, product premiums, inflation assumptions or gross-margin expectations may not be achieved, that Chinese or other international suppliers may reduce prices, that logistics costs may change or that product pricing may not offset changes in operating costs, energy costs, labor costs, raw-material costs or financing costs. Competitive Risks: Risks arising from established global solar glass producers and new entrants, including pricing pressure, technological competition, scale advantages, overcapacity in parts of the value chain, import competition and the presence of larger, better-capitalized competitors. Technology & Product Risks: Risks that antimony-free solar glass, patterned solar glass, glass-glass module formats, bifacial module applications, fused silica, laser-based purification or other advanced materials strategies may face technical challenges, qualification delays, product-performance issues, adoption barriers or slower-than-expected market acceptance. Resource & Feedstock Risks: Risks that the quality, consistency, recoverability, processing behavior or suitability of silica from the Santa Maria Eterna project or other relevant feedstock sources may vary over time, may require additional testing, ongoing quality control or may not meet evolving technical, commercial or customer-specific requirements. Sand Metallurgy & Process Risks: Risks that further sand metallurgy, processing flow confirmation, beneficiation assumptions, quality-control requirements or product-specification work may identify additional technical requirements, costs, delays or constraints that could affect project economics, plant design or customer acceptance. Infrastructure & Logistics Risks: Risks related to transportation, roads, ports, export logistics, packaging, natural gas availability, grid access, energy infrastructure, utility connections, water availability, supply-chain constraints, contractor performance and broader infrastructure dependencies that could affect project timelines, costs or operating reliability. Energy & Utility Risks: Risks that electricity, natural gas, LPG backup, on-site photovoltaic generation or other utility assumptions may differ from expectations, that energy prices may increase, that infrastructure may not be available on expected terms or timelines or that utility contracts may not be finalized on terms consistent with the BFS. BDR Trading & Capital Markets Risks: Risks that the Sponsored BDR program and B3 listing may not achieve the anticipated benefits, that Brazilian investor participation may be lower than expected, that liquidity may remain limited, that arbitrage between B3 and the TSX Venture Exchange may not function as expected, that cross-market settlement or custody processes may create delays or constraints or that BDR-related share custody may affect trading dynamics, float, liquidity, valuation or price discovery. BDR Access & Investor Eligibility Caution: Statements regarding the Company’s BDR listing on B3, potential Brazilian investor participation, market access, liquidity, arbitrage, custody mechanics or institutional interest are subject to market, regulatory, operational and investor-eligibility factors. The existence of a BDR trading facility does not guarantee increased demand, liquidity, valuation support, institutional participation or favorable trading dynamics in Brazil, Canada or any other market. Share Price & Liquidity Risks: Risks related to share price volatility, trading liquidity, investor sentiment, promotional activity, market awareness, small-cap market conditions, Canadian and Brazilian trading dynamics and the possibility that capital markets may not recognize or value the Company’s milestones as expected. Phase 2 Expansion Risks: Risks that the potential second production line may not be advanced, financed, approved, permitted, built or operated, that Phase 1 may not provide the expected platform benefits, that shared infrastructure advantages may not materialize or that demand, financing, permitting, board approval or market conditions may not support future expansion. Macroeconomic & Geopolitical Risks: Risks related to inflation, interest rates, exchange-rate volatility, energy prices, commodity prices, geopolitical instability, trade policies, tariffs, import restrictions, supply-chain disruptions, political developments in Brazil or other jurisdictions and broader economic uncertainty that may impact financing, construction, operations or market conditions. Energy Market & Policy Risks: Risks that changes in energy policy, solar incentives, net-metering rules, distributed-generation frameworks, industrial policy, local-content rules, renewable-energy targets, fossil fuel pricing dynamics or broader energy-transition policies may influence the pace of solar adoption and the overall market opportunity. Environmental & ESG Risks: Risks that environmental, social or governance considerations may impose additional costs, constraints or delays or that anticipated ESG advantages, including antimony-free product positioning, local production, reduced logistics exposure or lower-carbon manufacturing assumptions, may not translate into expected commercial or financial benefits. Foreign Exchange & Taxation Risks: Risks related to foreign-exchange volatility, differences between USD, CAD, BRL and EUR exposures, local taxation, VAT, duties, incentives, transfer pricing, cash-flow treatment, inflation, depreciation assumptions and the possibility that tax or currency outcomes may differ from those assumed in project planning. Operational Ramp-Up Risks: Risks that the plant may not ramp up according to the schedule, yield assumptions, production volumes, quality targets, cost profile or efficiency improvements assumed in the BFS and that startup, commissioning, workforce training, equipment performance or customer qualification may take longer or cost more than expected. Force Majeure & External Events: Risks arising from natural disasters, extreme weather, pandemics, labor disruptions, civil unrest, political instability, accidents, equipment failures, supply interruptions, contractor disruptions or other events beyond the Company’s control. Comparative Information, Valuation Metrics & Non-Equivalence Caution: References in this report to other companies, mining projects, feasibility studies, preliminary economic assessments, development-stage assets, NPV, IRR, CAPEX, payback periods, margins, production profiles, market capitalizations or other financial or technical metrics are provided for illustrative context only and should not be relied upon independently. Such comparisons may not be directly comparable to Homerun, its proposed solar glass manufacturing facility or its broader business strategy. Mining projects and industrial manufacturing projects may differ materially in geology, permitting, financing structure, commodity exposure, operating risk, construction risk, market dynamics, cost structure, customer concentration, taxation, jurisdictional framework, technical requirements and revenue model. No comparison should be interpreted as implying that Homerun will achieve similar results, valuations, financing outcomes, construction timelines, operating performance or market recognition. Accordingly, readers should not place undue reliance on forward-looking information. Rockstone and the author of this report do not undertake any obligation to update any statements made in this report except as required by law. Past performance, comparisons to other companies, projects, commodities, technologies, jurisdictions, feasibility studies, capital-market events or industry trends are provided for illustrative purposes only and should not be considered indicative of future results.

Disclosure of Interest and Advisory Cautions: Nothing in this report should be construed as a solicitation to buy or sell any securities mentioned. Rockstone, its owners and the author of this report are not registered broker-dealers or financial advisors. Before investing in any securities, you should consult with your financial advisor and a registered broker-dealer. Never make an investment based solely on what you read in an online or printed report, including Rockstone’s report, especially if the investment involves a small, thinly-traded company that isn’t well known. The author of this report, Stephan Bogner, is paid by Homerun Resources Inc. On September 8, 2025, Homerun announced that the company “entered into an agreement with Rockstone Research to provide marketing services to the company”, and that “Rockstone Research is an arm’s-length marketing firm and has been engaged for an initial three-month term for total consideration of $25,000, which is payable up front. The company does not propose to issue any securities to Rockstone in consideration for the services to be provided to the company.” The author owns equity of Homerun and thus will profit from volume and price appreciation of the stock. This also represents a significant conflict of interest that may affect the objectivity of this reporting. The author may buy or sell securities of Homerun (or comparable companies) at any time without notice, which may give rise to additional conflicts of interest. Overall, multiple conflicts of interests exist. Therefore, the information provided in this report should not be construed as a financial analysis or recommendation but as an advertisement. This report should be understood as a promotional publication and does not replace individual investment advice. Rockstone’s and the author’s views and opinions regarding the companies that are featured in the reports are the author‘s own views and are based on information that was received or found in the public domain, which is assumed to be reliable. Rockstone and the author have not undertaken independent due diligence of the information received or found in the public domain. Rockstone and the author of this report do not guarantee the accuracy, completeness, or usefulness of any content of this report, nor its fitness for any particular purpose. Lastly, Rockstone and the author do not guarantee that any of the companies mentioned in the reports will perform as expected, and any comparisons that were made to other companies may not be valid or come into effect. Please read the entire Disclaimer carefully. If you do not agree to all of the Disclaimer, do not access this website or any of its pages including this report in form of a PDF. By using this website and/or report, and whether or not you actually read the Disclaimer, you are deemed to have accepted it. Information provided is educational and general in nature and should not be interpreted as personalized investment, financial, legal, tax or professional advice. Data, tables, figures and pictures, if not labeled or hyperlinked otherwise, have been obtained from Stockwatch.com, Tradingview.com, Homerun Resources Inc. and the public domain. The cover picture has been obtained and licenced from 123rf.com.