In a fireside chat with Water Tower Research on March 24, Homerun CEO Brian Leeners laid out the company’s strategy to build a vertically integrated silica platform in Brazil, with solar glass as the lead commercial opportunity and advanced materials adding further upside.

The discussion covered district-scale consolidation at Santa Maria Eterna, third-party validation for antimony-free solar glass, UC Davis bench work in fused silica and silicon carbide, expanding offtake discussions and the milestones that could move Homerun toward a BFS (Bankable Feasibility Study) and future solar glass production.

You are currently viewing a placeholder content from YouTube. To access the actual content, click the button below. Please note that doing so will share data with third-party providers.

More InformationKey Takeaways:

- Homerun’s silica resource stands out for its high purity.

- That matters because purity drives both quality and cost.

- It may reduce the need for chemical processing.

- It also supports the potential production of antimony-free solar glass.

- That could lower input costs and improve margins.

- Brian emphasized that consolidating the Santa Maria Eterna Silica Sand District was a foundational step.

- Full district control supports scale.

- It improves supply security.

- It may also reduce logistics costs and strengthen project economics.

- Third-party validation confirmed the silica is suitable for high-quality solar glass.

- That is a major technical milestone.

- It strengthens the case for a BFS.

- It also moves Homerun closer to a future solar glass plant in Bahia.

- Brian also highlighted the UC Davis work.

- Bench trials showed progress in fused silica and silicon carbide.

- Homerun has also filed a patent tied to laser purification of silica sand.

- The focus is not just scientific proof. The focus is scalable economics.

- A key part of the strategy is using off-the-shelf equipment.

- That could make scale-up faster.

- It could make commercialization cheaper.

- It could also reduce execution risk.

- Solar glass remains the main industrial silica opportunity, but Brian also pointed to larger long-term upside in advanced materials.

- That includes fused silica for optics, photonics, data storage and other technology applications.

- In other words: Homerun is not chasing a single end market.

- Brian said the company’s verticals are being advanced in parallel.

- Homerun is not waiting for one revenue stream to mature before building the next.

- It is working to create multiple paths to commercialization.

- On the commercial side, Brian said Homerun has already lined up offtake interest beyond initial planned plant throughput.

- He also pointed to ongoing discussions with module makers outside Brazil.

- He mentioned direct talks with U.S. government officials focused on supply chain development.

- For investors, the main milestone now is scaling revenue.

- Resource consolidation was the first step.

- Commercial execution is the next step.

- Brian said progress should increasingly be measured by sales growth, throughput and cash flow.

- His broader message was clear: Homerun is not positioning itself as just another silica supplier.

- It is working to build a broader silica platform tied to solar glass, advanced materials and the energy transition.

Bottom Line

Homerun is moving beyond the raw materials story and positioning itself as a potential supplier into higher-value solar glass and advanced silica markets.

Rather than stopping at resource extraction, the company is working to convert its high-purity silica sand into products with stronger margins, broader industrial relevance and greater long-term strategic value.

Solar glass is the clearest near-term path, while fused silica, silicon carbide and other advanced applications provide added upside as the platform develops.

From Silica Sand to Optical Glass: UC Davis Research Highlights Homerun’s Path Into High-Value Silica Applications

At IOCO 2026, Dr. Subhash Risbud of UC Davis presented an overview of Homerun’s ongoing research collaboration with the university, explaining how the company’s silica sand is being used in work aimed at producing fused silica optical glass, a high-value material used in advanced lenses, lasers, photonics and other precision technologies.

You are currently viewing a placeholder content from YouTube. To access the actual content, click the button below. Please note that doing so will share data with third-party providers.

More InformationThe focus of the work is both technically ambitious and commercially relevant: Turning quartz/silica sand into fused silica optical glass.

For investors, the significance is straightforward. This is not about selling ordinary sand into low-value markets, but about investigating whether Homerun’s high-purity silica sand feedstock can become the starting point for a much more valuable end product used in advanced industrial and technology applications.

Fused Silica as a Higher-Value End Product

Fused silica is a very pure and highly specialized form of glass made from silica derived from quartz. It is valued for its exceptional clarity, thermal resistance, chemical stability and performance under demanding conditions.

These properties make it important in applications such as:

- precision optical lenses

- high-power laser systems

- photonics components

- specialty glass products

- advanced industrial and scientific equipment

In short: Fused silica sits far above raw silica sand in the value chain.

A Faster Route From Sand to Optical Glass

Dr. Risbud explained that his team at UC Davis has been working with silica sand supplied by Homerun for roughly 2 years, with the goal of developing faster and more efficient ways to make fused silica glass.

That matters because traditional fused silica production can be slow, energy-intensive and expensive. Silica is difficult to melt and process because of its high melting point and viscosity. The UC Davis team is therefore testing ways to reduce production time while still achieving the quality required for demanding optical applications.

In simple terms: The research is exploring a better, faster and potentially more economical route from silica sand to high-grade optical glass.

Shorter Processing Times & Future Commercial Relevance

One of the most important messages in the presentation was that conventional methods can take many hours to produce fused silica, while the techniques under investigation may be able to reduce that to minutes in some cases.

That kind of time reduction could eventually become commercially meaningful. Shorter processing times may support:

- Improved throughput

- Lower energy use

- Reduced production costs

- Better scalability for future manufacturing

While this work remains in the R&D stage, the direction is highly relevant from an investor standpoint because it addresses one of the central questions of commercialization: Whether high-value fused silica can be made faster and more efficiently from a suitable silica sand source.

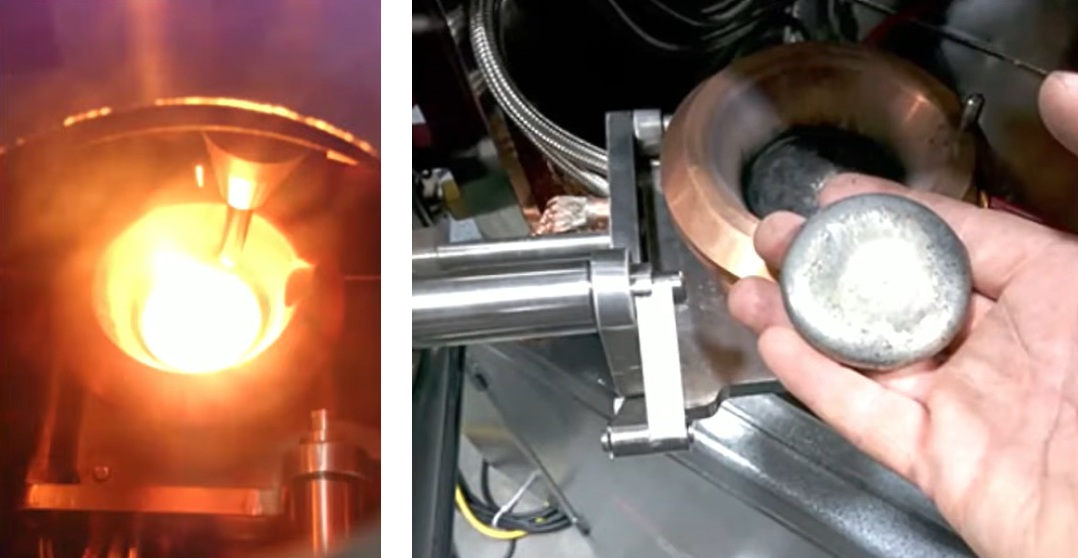

Flash Joule Heating: Rapid Thermal Processing

One of the most interesting techniques discussed was Flash Joule Heating, a process that uses a rapid burst of intense heat.

Because silica itself is an electrical insulator, the research team developed a setup in which the silica is placed inside a conductive surrounding material that helps transfer heat quickly. Dr. Risbud explained that this process was able to reach temperatures of about 2,000°C, which is above silica’s melting point, and produced early glass results in only a few minutes.

For investors, this is notable because it suggests the possibility of dramatically faster fused silica production than conventional furnace-based approaches.

Arc Welding: Early-Stage Glass Formation Tests

The team is also experimenting with an arc welding-based process in which silica rock pieces are exposed to a high-temperature arc inside a controlled setup.

Dr. Risbud made clear that this work is still at an early stage, with partially melted material seen so far. However, the goal is clear: To ultimately produce transparent fused silica glass discs quickly and efficiently.

This is not yet a finished solution, but it represents another promising route being tested.

Spark Plasma Sintering: Fast Densification Methods

Another method highlighted was Spark Plasma Sintering, a technique that uses electrical pulses and pressure to densify powdered material much faster than traditional methods.

Dr. Risbud noted that this is a technology his group has worked with successfully for many years. In this process, electrical pulses are first applied to the powder, followed by heating and compression, allowing dense discs to be formed in minutes rather than hours.

Although this is not identical to full glass melting, it is part of the broader toolkit being used to accelerate materials processing.

Microwave Heating: Additional Experimental Pathways

The team has also begun exploring whether silica can be processed using Microwave Heating, with protective surrounding materials used to help control the system.

This work appears to be in the earliest stages, but it shows the breadth of the research effort and the willingness to test multiple pathways toward the same commercial objective.

Purity & Feedstock Quality

A major theme in the presentation was purity. For fused silica optical glass, impurities matter. Even small amounts of unwanted material can affect clarity, performance and suitability for high-end applications.

That is why the UC Davis team is not only studying melting methods, but also working on ways to improve the purity of the quartz feedstock before processing.

Dr. Risbud described a laser-based purification approach as an alternative to traditional chemical treatments such as acid washing and flotation. According to the presentation, this laser route has already achieved very high silica purity levels, with results reaching 99.99% in some tests.

That is strategically important because it points to a broader value-upgrading pathway:

Silica sand → higher purity silica → fused silica optical glass

That is exactly the kind of vertical progression investors want to see when evaluating whether a raw materials story can evolve into an advanced materials story.

Strategic Relevance for Homerun

The most important takeaway from the presentation is that Homerun’s silica sand is not just being discussed in theory, but that it is being actively used in a university-based research program focused on advanced materials processing.

This matters for several reasons:

- It supports the idea that Homerun’s feedstock may be suitable for higher-value downstream applications.

- It connects the company to real R&D aimed at solving practical production challenges such as speed, purity and process efficiency.

- It places Homerun within a conversation that extends well beyond industrial minerals and into areas like optics, photonics, advanced manufacturing and specialty glass.

That is where the commercial upside becomes more interesting.

A Broader Advanced Materials Opportunity

For many resource companies, the story ends at extraction and sale of raw material.

What makes this work more compelling is that Homerun appears to be exploring something more ambitious: How to participate in downstream value creation.

If the company’s silica sand can be purified and processed into fused silica suitable for advanced optical and photonics applications, then the long-term opportunity could look very different from a conventional sand or silica story.

That is why Dr. Risbud’s presentation matters. It suggests that Homerun’s silica sand resource may have relevance not only in traditional silica markets, but also in future high-margin applications linked to precision manufacturing and next-generation technology supply chains.

Bottom Line

In a nutshell, Dr. Risbud’s message was this: Homerun’s quartz sand is being tested as the starting material for high-value fused silica optical glass, and UC Davis is working on faster and potentially more efficient ways to make that happen.

That does not mean the process is fully commercial today, but it does mean Homerun is taking steps that could move its silica sand feedstock beyond the raw materials category and into advanced materials applications with much greater strategic and economic significance.

Company Details

Homerun Resources Inc.

#2110 – 650 West Georgia Street

Vancouver, BC, V6B 4N7 Canada

Phone: +1 844 727 5631

Email: info@homerunresources.com

www.homerunresources.com

ISIN: CA43758P1080 / CUSIP: 43758P

Shares Issued & Outstanding: 75,551,618

Canada Symbol (TSX.V): HMR

Current Price: 0.88 CAD (03/27/2026)

Market Capitalization: 67 Million CAD

Germany Ticker / WKN: 5ZE / A3CYRW

Current Price: 0.54 EUR (03/27/2026)

Market Capitalization: 41 Million EUR

Stephan Bogner

Contact

Rockstone News & Research

Stephan Bogner (Dipl. Kfm., FH)

Müligässli 1, 8598 Bottighofen

Switzerland

Phone: +41-71-5896911

Email: info@rockstone-news.com

Disclaimer and Information on Forward Looking Statements: Rockstone and Homerun Resources Inc. (“Homerun“) caution investors that any forward-looking information provided herein is not a guarantee of future results or performance, and that actual results may differ materially from those in forward-looking information as a result of various factors. The reader is referred to Homerun’s public filings for a more complete discussion of such risk factors and their potential effects, which may be accessed through its documents filed on SEDAR+ at www.sedarplus.ca. All statements in this report, other than statements of historical fact, should be considered forward-looking statements. Much of this report is comprised of statements of projection, interpretation and expectation. Such statements involve known and unknown risks, uncertainties and other factors that may cause actual results, performance, achievements or events to differ materially from those anticipated in these forward-looking statements. There can be no assurance that such statements will prove to be accurate, as actual results and future events could differ materially from those anticipated in such statements. Forward-looking statements in this report include expectations related to the commercial, strategic and market implications of statements made by Homerun Resources Inc. management during the March 24, 2026 Water Tower Research fireside chat and the March 27, 2026 presentation by Dr. Subhash Risbud at the 1st International Online Conference on Optics (IOCO 2026). Forward-looking statements include expectations regarding the Company’s strategy to build a vertically integrated silica platform in Brazil, including assumptions that Homerun may successfully advance resource ownership, district-scale consolidation, logistics, distribution, customer relationships, downstream processing, technical validation and commercialization into an integrated industrial platform. Forward-looking statements also include expectations related to the Santa Maria Eterna high-purity silica sand district, including assumptions that district-scale consolidation may support scale, supply security, project economics, lower logistics costs and broader strategic flexibility over time. Additional forward-looking statements include expectations regarding the suitability of the Company’s silica sand for solar glass applications, including assumptions that third-party validation and internal technical work may continue to support the view that Homerun’s feedstock is suitable for high-quality, antimony-free solar glass and that such suitability may translate into commercial relevance, reduced processing steps, lower input costs, improved margins, premium positioning or competitive differentiation. Forward-looking statements further include expectations regarding a potential bankable feasibility study, including assumptions that technical validation, resource control, customer engagement, commercial planning and project development work may support the preparation, completion and positive conclusions of a bankable feasibility study and may advance the Company toward a future solar glass manufacturing facility in Bahia, Brazil. Such statements do not represent a commitment that any feasibility study will be completed on a particular timeline, that it will reach favorable conclusions or that any plant will be financed, constructed or operated successfully. Forward-looking statements also include expectations regarding Homerun’s broader advanced materials strategy, including assumptions that the Company’s silica sand may support not only solar glass but also additional downstream products and markets such as fused silica, silicon carbide and other advanced silica-based materials. Statements in this report regarding fused silica optical glass, silicon carbide and other advanced applications are forward-looking to the extent they describe the Company’s future strategic positioning, potential commercial relevance, expected market opportunities, possible margin profile, scalability or long-term industrial significance. Forward-looking statements include assumptions that bench-scale work performed with UC Davis may continue to demonstrate technical progress, that such work may be scalable, economically viable and commercially relevant and that the Company may be able to translate laboratory results into pilot-scale, demonstration-scale or industrial-scale processes over time. Forward-looking statements also include assumptions that the Company’s silica sand may be purified and processed through thermal, laser-based, electrically driven or other methods in ways that may reduce conventional processing steps, improve economics, enhance purity levels, expand end-market applicability or support new product categories. Additional forward-looking statements include expectations related to Homerun’s filed patent applications and intellectual property strategy, including assumptions that patent-related work tied to laser purification or other processing methods may be granted, protected, enforceable, commercially meaningful or supportive of competitive advantage. Forward-looking statements also include expectations that the use of off-the-shelf equipment, standard industrial inputs or scalable processing methods may reduce execution risk, accelerate scale-up, lower capital intensity or improve the likelihood of commercial adoption. Such statements are inherently uncertain and depend on future engineering, market acceptance, financing, execution and regulatory outcomes. Forward-looking statements further include expectations regarding demand development, commercial rollout and customer adoption, including assumptions that Homerun may secure or expand offtake interest, convert discussions into binding agreements, establish broader B2B sales channels, engage module manufacturers in Brazil or internationally, support distribution growth and scale revenue over time. Such statements include assumptions that current or future customer interest may translate into actual sales, repeat business, volume growth or sustained market penetration and that planned plant throughput, customer demand and revenue growth may align with management expectations. Additional forward-looking statements include expectations regarding market relevance and macro tailwinds, including assumptions that solar glass, advanced silica materials, fused silica, silicon carbide, optics, photonics, data storage, energy transition infrastructure and other related sectors may continue to grow in ways supportive of the Company’s strategy. Forward-looking statements also include expectations regarding discussions with government bodies, industry counterparties and strategic partners, including assumptions that such discussions may improve supply chain positioning, support financing, accelerate project development, improve commercial visibility or contribute to future partnerships or sales. Forward-looking statements also include statements regarding vertical integration, commercialization milestones and performance measurement, including assumptions that the Company may successfully move from resource consolidation toward revenue generation and that future progress may be reflected in higher sales, throughput, cash flow, margins or broader industrial relevance. All such forward-looking statements are based on current expectations, estimates, assumptions and interpretations that are inherently subject to uncertainty and may differ materially from actual outcomes. Forward-looking statements are subject to risks and uncertainties including, but not limited to: Technical Validation Risks: Risks that third-party testing, bench-scale trials, academic collaborations or internal validation efforts may not continue to support current assumptions regarding silica purity, processability, suitability for solar glass, fused silica, silicon carbide or other downstream uses and that future results may be less favorable, less consistent or less commercially relevant than early-stage findings suggest. Scale-Up Risks: Risks that laboratory or bench-scale successes may not be replicated at pilot, demonstration or industrial scale and that technical processes which appear promising in small-scale settings may prove difficult, expensive, unreliable, energy-intensive or impractical to implement commercially. Process Development Risks: Risks that purification, melting, sintering, thermal-electric, arc, microwave, laser-based or other process routes may require additional optimization, may not achieve expected yields, may not maintain quality at scale, may depend on specialized conditions or may not provide the anticipated cost or speed advantages relative to conventional methods. Economic Viability Risks: Risks that any technically successful process may not be economically viable, may not outperform existing industry methods, may require higher-than-expected capital or operating expenditures or may fail to deliver acceptable returns, margins or payback periods. Feasibility Study Risks: Risks that a bankable feasibility study may be delayed, may not be completed, may identify technical or commercial shortcomings, may require material revisions to current strategy or may not support financing, plant construction or project execution on acceptable terms. Solar Glass Market Risks: Risks that anticipated demand for antimony-free or high-quality solar glass may develop more slowly than expected, may be affected by pricing pressure, technological change, trade policy, competing suppliers, substitute materials or overcapacity and may not support the commercial assumptions reflected in this report. Advanced Materials Market Risks: Risks that anticipated opportunities in fused silica, silicon carbide, optics, photonics, data storage, memory technologies, quantum computing or other advanced materials markets may not materialize on the scale or timeline expected, may be more competitive than anticipated or may require qualifications, certifications, product standards or customer acceptance thresholds that the Company is unable to meet. Resource and Feedstock Risks: Risks that the Company’s silica sand may not consistently exhibit the purity, grain size, mineralogy, recoverability, low-iron characteristics, processing behavior or downstream suitability assumed in this report and that variations in resource quality may impair commercial performance or technical outcomes. Antimony-Free Product Risks: Risks that the Company may not ultimately be able to produce antimony-free solar glass at commercial scale, that any such product may not achieve expected cost or pricing advantages or that customers may not assign premium value to that differentiation. Patent and Intellectual Property Risks: Risks that patent applications may not be granted, may be narrowed, challenged or circumvented and may not provide meaningful protection, exclusivity or commercial leverage. Commercialization Risks: Risks that customer discussions, offtake interest, module maker engagement, strategic outreach or government-related conversations may not result in binding agreements, recurring sales, strategic support or meaningful commercial outcomes. Counterparty and Partnership Risks: Risks that current or future partners, distributors, research institutions, contractors, customers, licensors or strategic counterparties may not perform as expected, may terminate or modify relationships or may not commit the capital, resources or time necessary to advance shared objectives. Revenue Scaling Risks: Risks that the Company may be unable to scale revenue in the manner or timeframe anticipated and that sales growth, throughput, working capital conversion, customer onboarding or repeat ordering may be delayed, uneven or absent. Execution Risks: Risks associated with management execution, staffing, engineering, procurement, scheduling, operating discipline, contractor performance, quality control, product consistency, order fulfillment, logistics coordination and broader organizational capacity as the Company moves from development into commercialization. Equipment and Supply Chain Risks: Risks that off-the-shelf equipment may not perform as expected, may require modification, may not be available when needed or may not support efficient scale-up and that equipment procurement, fabrication, lead times, spare parts, imported components or supply chain disruptions may impair project timelines or economics. Infrastructure and Logistics Risks: Risks related to road access, port access, energy availability, water supply, transport capacity, freight conditions, warehousing, local infrastructure and site readiness, any of which could impair timely and cost-effective execution. Regulatory and Permitting Risks: Risks relating to mining permits, land access, environmental approvals, industrial permits, construction approvals, tax matters, trade policy, export controls, import restrictions, labor rules, health and safety requirements and other regulatory frameworks in Brazil, North America or other relevant jurisdictions. Financing and Capital Risks: Risks that the Company may be unable to secure sufficient capital on acceptable terms to fund studies, pilot work, plant design, construction, working capital, commercialization activities, downstream development or broader corporate initiatives. Competitive Risks: Risks arising from competing silica resources, established glass producers, integrated industrial groups, substitute materials, new entrants, lower-cost producers or better-capitalized competitors that may reduce the Company’s pricing power, market access or strategic relevance. Market and Pricing Risks: Risks that silica sand, solar glass, fused silica, silicon carbide or related products may face adverse pricing, weak customer economics, volatile end markets, changing procurement strategies or fluctuating energy, freight, labor and input costs. Government and Policy Risks: Risks that supply chain support, industrial policy initiatives, domestic manufacturing incentives, renewable energy policies or trade frameworks in Brazil, the United States or elsewhere may change, weaken or fail to benefit the Company. Environmental and ESG Risks: Risks that operations or proposed downstream developments may face environmental constraints, permitting delays, community opposition, water-use restrictions, emissions-related issues, land disturbance concerns, reclamation costs or broader ESG-related scrutiny. Macroeconomic and Currency Risks: Risks related to inflation, interest rates, exchange-rate volatility, recessionary pressures, capital markets conditions, sovereign risk, commodity prices, geopolitical instability and broader economic uncertainty that may affect financing, customer demand, project economics or investor sentiment. Force Majeure and External Event Risks: Risks arising from extreme weather, flooding, drought, fire, natural disaster, epidemic, labor disruption, civil unrest, cyber incidents or other events beyond the Company’s control. Liquidity and Market Trading Risks: Risks relating to limited trading liquidity, share price volatility, speculative trading behavior or shifts in investor sentiment that may be unrelated to underlying operating progress. Accordingly, readers should not place undue reliance on forward-looking information. Rockstone and the author of this report do not undertake any obligation to update any statements made in this report except as required by law. Past performance, comparisons to other companies, projects, commodities, technologies, jurisdictions or market themes and references to industry trends or future addressable markets are provided for illustrative purposes only and should not be considered indicative of future results.

Disclosure of Interest and Advisory Cautions: Nothing in this report should be construed as a solicitation to buy or sell any securities mentioned. Rockstone, its owners and the author of this report are not registered broker-dealers or financial advisors. Before investing in any securities, you should consult with your financial advisor and a registered broker-dealer. Never make an investment based solely on what you read in an online or printed report, including Rockstone’s report, especially if the investment involves a small, thinly-traded company that isn’t well known. The author of this report, Stephan Bogner, is paid by Homerun Resources Inc. On September 8, 2025, Homerun announced that the company “entered into an agreement with Rockstone Research to provide marketing services to the company”, and that “Rockstone Research is an arm’s-length marketing firm and has been engaged for an initial three-month term for total consideration of $25,000, which is payable up front. The company does not propose to issue any securities to Rockstone in consideration for the services to be provided to the company.” The author owns equity of Homerun and thus will profit from volume and price appreciation of the stock. This also represents a significant conflict of interest that may affect the objectivity of this reporting. The author may buy or sell securities of Homerun (or comparable companies) at any time without notice, which may give rise to additional conflicts of interest. Overall, multiple conflicts of interests exist. Therefore, the information provided in this report should not be construed as a financial analysis or recommendation but as an advertisement. This report should be understood as a promotional publication and does not replace individual investment advice. Rockstone’s and the author’s views and opinions regarding the companies that are featured in the reports are the author‘s own views and are based on information that was received or found in the public domain, which is assumed to be reliable. Rockstone and the author have not undertaken independent due diligence of the information received or found in the public domain. Rockstone and the author of this report do not guarantee the accuracy, completeness, or usefulness of any content of this report, nor its fitness for any particular purpose. Lastly, Rockstone and the author do not guarantee that any of the companies mentioned in the reports will perform as expected, and any comparisons that were made to other companies may not be valid or come into effect. Please read the entire Disclaimer carefully. If you do not agree to all of the Disclaimer, do not access this website or any of its pages including this report in form of a PDF. By using this website and/or report, and whether or not you actually read the Disclaimer, you are deemed to have accepted it. Information provided is educational and general in nature. Data, tables, figures and pictures, if not labeled or hyperlinked otherwise, have been obtained from Stockwatch.com, Tradingview.com, Homerun Resources Inc. and the public domain. The cover picture has been obtained and licenced from 123rf.com.